The cost of Illinois’ broken pension systems: per-employee retirement contributions 4 times the private sector

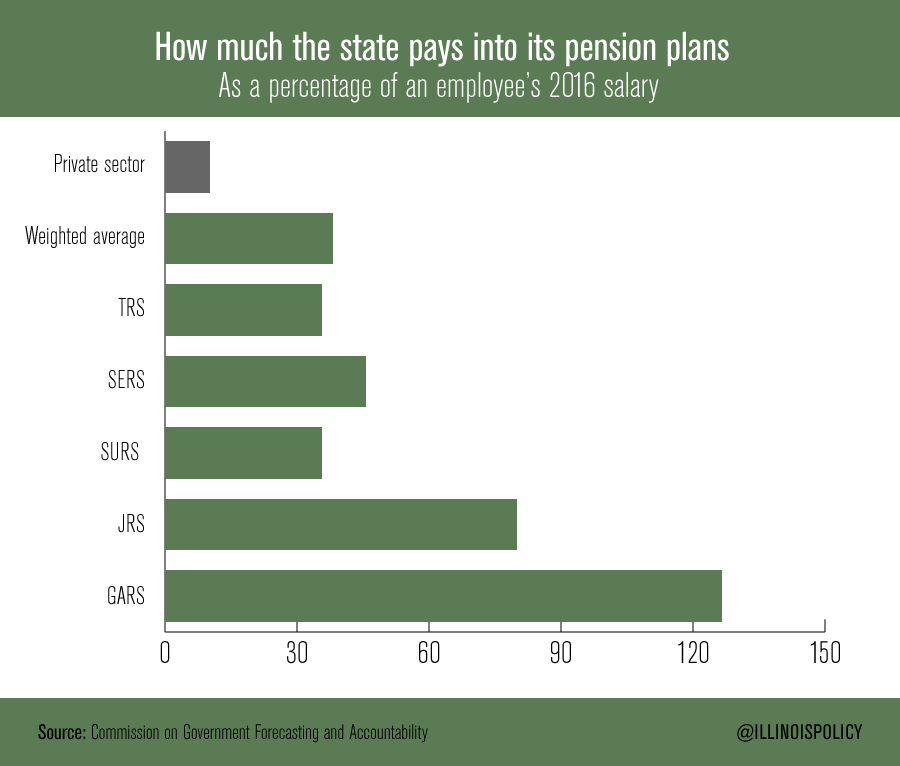

Illinois state government contributes the equivalent of 35 to 127 percent of government-worker salaries to keep its pension systems above water.

Imagine a company contributing the equivalent of 30 to 40 percent of its workers’ salaries each year to worker-retirement costs alone. No business could sustain that level of costs and compete, let alone survive.

In fact, the market is littered with companies bankrupted by the ballooning costs of traditional pension plans.

But that’s precisely what the Illinois government is trying to get away with. Illinois’ five state-run pension plans are so deep in the hole that the state – the employer – is now contributing the equivalent of 35 to 127 percent of its government-worker salaries just to keep its pension systems afloat. It’s simply unsustainable.

On average, the government contributes to its pension plans the equivalent of 38 percent of each worker’s salary in order to meet the state’s pension obligations. Those contributions cover not only the benefits workers accrue today, but also the shortfall created by the inherent flaws of Illinois’ politician-run pension system.

For example, to keep both the Teachers’ Retirement System, or TRS, and the State Universities Retirement System, or SURS, afloat, the state contributes the equivalent of 35 percent of an employee’s salary each year.

Compare that to the private sector, where the majority of companies have modernized retirements by transitioning to defined-contribution plans like 401(k)s. A typical company today contributes the equivalent of 9 to 10 percent of a worker’s salary each paycheck – some 3 to 4 percent toward the employee’s 401(k) and another 6.2 percent toward his or her Social Security.

To see just how out of control Illinois pensions have become, look at legislator pensions and their General Assembly Retirement System, or GARS. Not only does the state pay its legislators high salaries for their part-time work, but it must also contribute an amount equivalent to 127 percent of their salaries just to fund their pension system. Effectively, taxpayers today pay twice for one set of legislators.

The state, by keeping its antiquated pension plan, is flirting with insolvency.

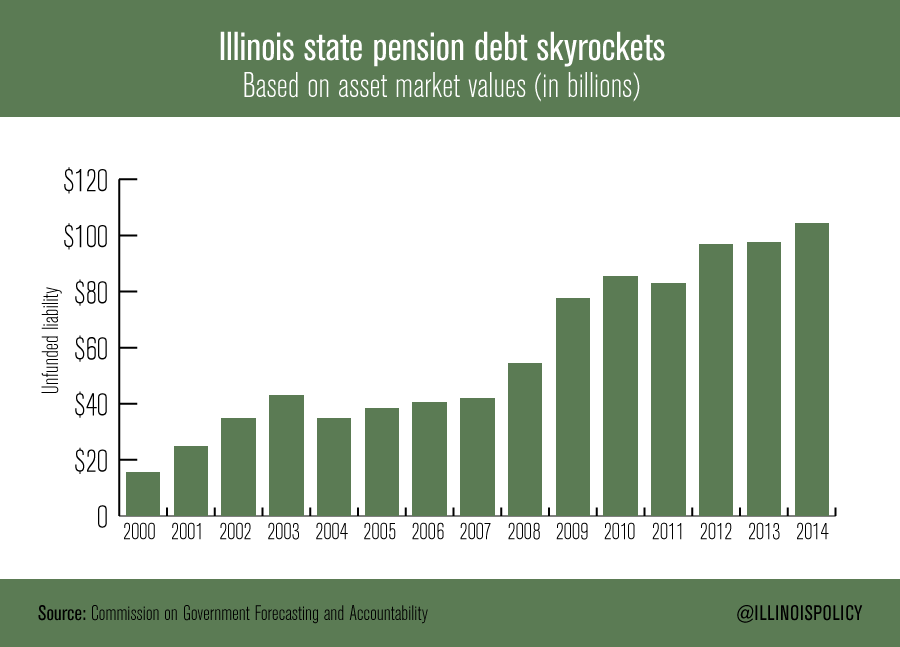

Illinois’ pension debt is now so large the state has no credible way of paying it down. In 2000, the state had less than $16 billion in pension debt. That amount has skyrocketed to nearly $105 billion – or $111 billion based on smoothed asset values – in 2014. No amount of tax hikes and pension bond issues have been able to stop the massive increase in Illinois’ pension debt.

Politicians have run government-worker pensions and the state that funds them into the ground, which puts all eyes on the state Supreme Court’s upcoming ruling on Illinois’ recently passed pension reforms.

Opponents of pension reform would cheer the Supreme Court’s rejection of the law. But that rejection would do nothing to fix Illinois’ pension crisis or reduce its debt.

In the end, only real reforms, whether legislated or negotiated, will fix Illinois’ insolvency.