The problem

Education funding for downstate and suburban pre-K-12 schools – i.e., all Illinois school districts outside of Chicago – is one of the state’s highest priorities. It’s also one of the only expenditures where increased funding is almost guaranteed year after year, even in times of fiscal crises.

Illinois is in such a crisis now. The 2016 budget is currently $4 billion out-of-balance, the state’s credit rating has fallen to within four notches of junk status, and the state’s pension shortfall has reached an all-time high of $111 billion.1,2,3

Despite the above issues, 2016’s education spending has already been appropriated and passed into law – and has actually been increased over last year.4

However, increasing the dollar amount spent on education does not guarantee that more money will be spent on teaching children.

That’s because state education spending is made up of much more than what is spent daily to run Illinois schools. It also includes the annual contributions to teachers’ retirements and retiree health care. And, while not part of the budget for education, Illinois must also pay down the portion of the state’s annual pension obligation bond payments (POBs) allotted to the Teachers’ Retirement System, or TRS, which covers all Illinois elementary- and secondary-school teachers outside of Chicago. In 2003, 2010 and 2011, Illinois issued POBs to pay for annual contributions into the pension system. Now the state has to pay back those bonds over a period of time, which adds additional costs to teacher-retirement spending.

Unfortunately, these mounting, nonoperating retirement costs are dramatically siphoning funds away from classrooms.

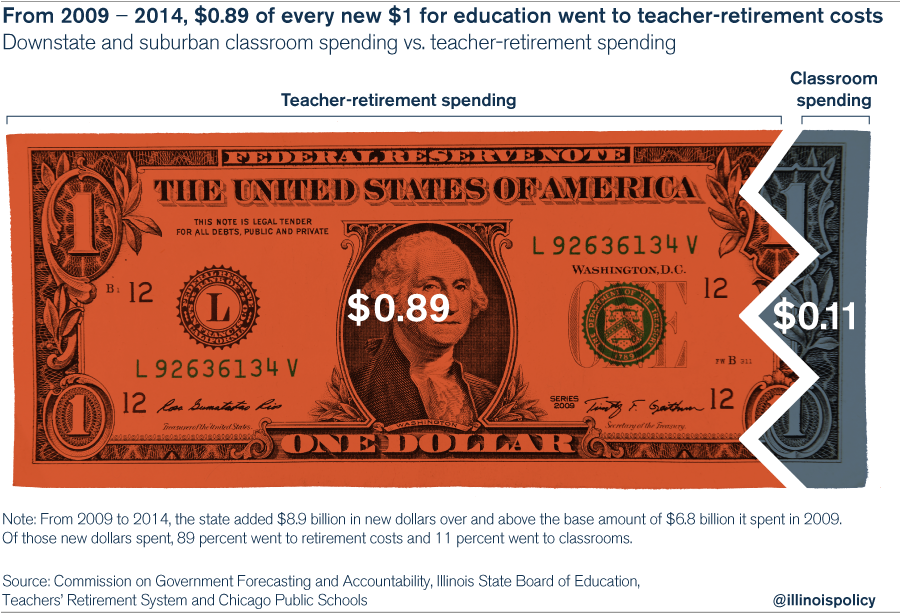

In fact, if you look at total education spending from 2009 to 2014, the state added $8.9 billion in new dollars over and above the base amount of $6.8 billion it spent in 2009. Of those new dollars spent, 89 percent went to pay for retirement costs. Just 11 percent made it to the classroom.

The money that politicians poured into education over the last several years has really been funding pensions instead.

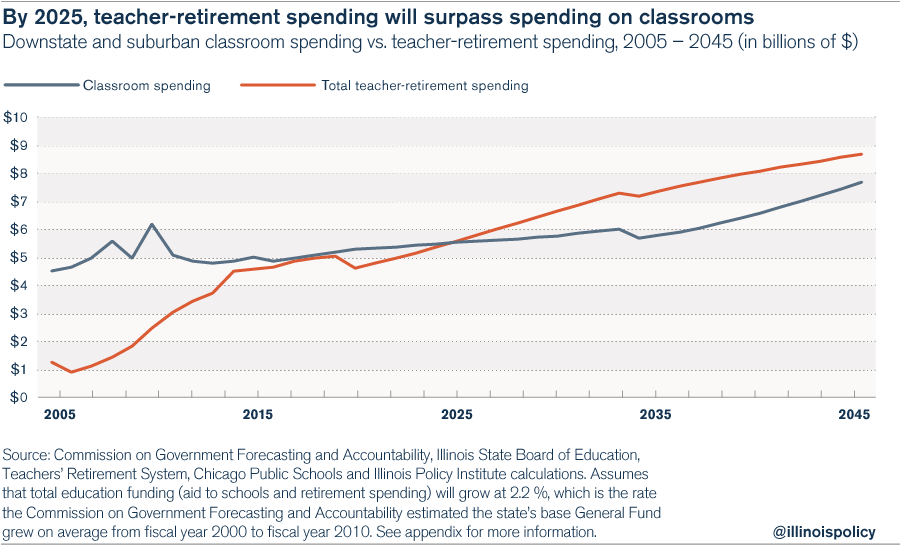

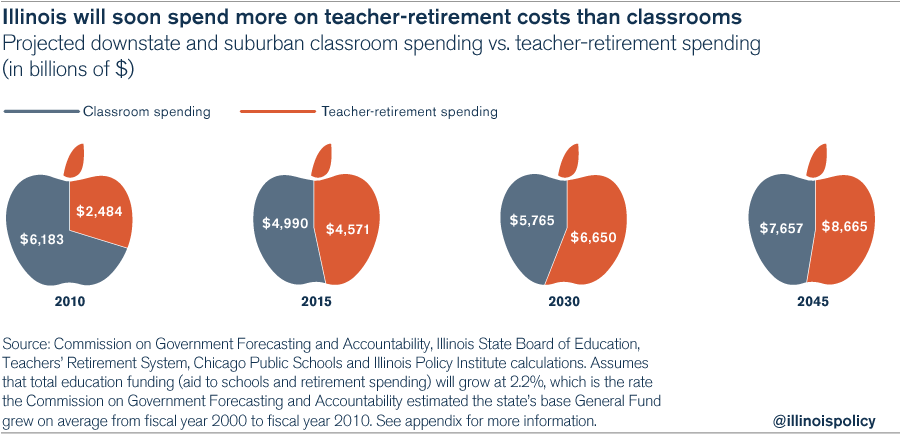

Spending on retirement costs already rivals the total amount spent on classrooms. From 2015 to 2019, retirement spending will almost equal classroom spending. And by 2025, if spending continues along its current trajectory, the amount spent on retirement costs will surpass that spent on classrooms.

By the time a child born in 2015 enters the sixth grade, the state will be spending more on teacher retirements than on aid to pre-K-12 schools.

Even assuming that TRS’s unfunded liability doesn’t grow progressively worse as it has in years past, retirement costs will consistently make up more than 50 percent of all education spending through 2045.

However, if TRS’s unfunded liabilities do continue to increase, as recent pension-fund history would indicate, retirement costs will crowd out funds for downstate and suburban classroom spending even further.

This crowding out will drastically affect local school districts’ operational budgets – especially poorer districts that rely heavily on state funding.

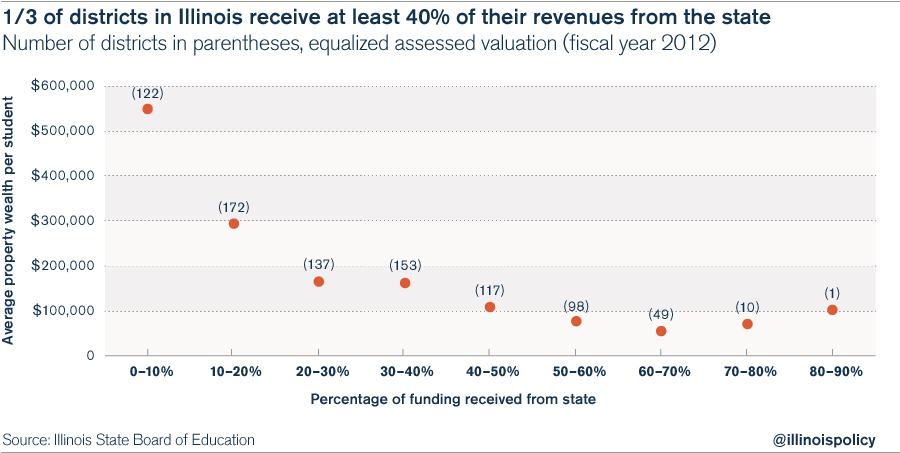

The amount of property wealth in each school district determines the amount of taxes it can raise locally to finance its education needs. The less property wealth a district has, the more state funds it receives. The neediest districts, then, receive a majority of their funding from the state.

While the vast majority of Illinois school districts draw most of their funding from local sources, almost a third of the districts in Illinois receive at least 40 percent of their revenues from the state.5

Without real pension reform, hundreds of schools across those districts may have to cut programs, increase class sizes or lay off teachers as more and more new state dollars are directed away from operations toward retirements.

And as districts with higher levels of state funding generally serve lower-income and minority communities, those groups will end up being the most negatively affected by the growth in retirement spending.

Crowd-out culprits

The pension crisis

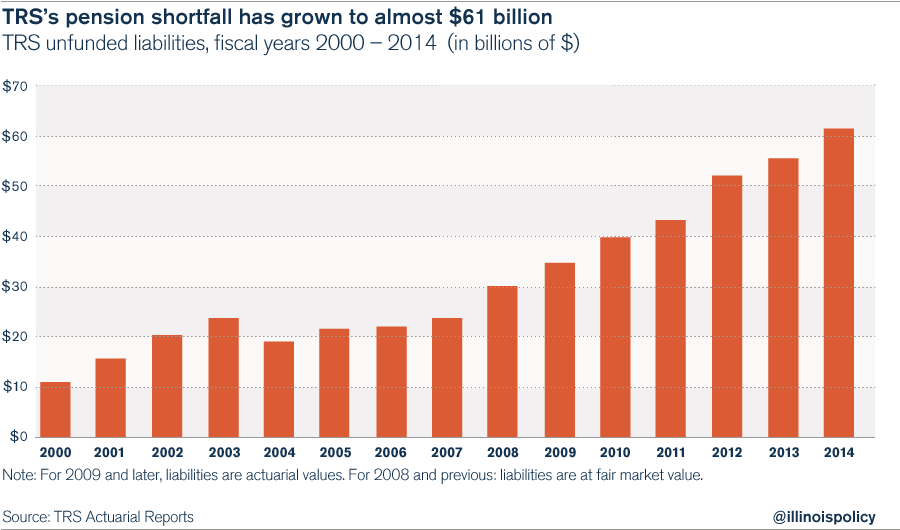

Contributing disproportionately to its general budget crisis is Illinois’ worsening government-pension funding crisis. The shortfall from the state’s pension funds reached an all-time high of $111 billion in 2014, $62 billion of which was attributable to TRS.6

The crisis in TRS has been building for years. In 2000, TRS’s pension shortfall equaled just $15 billion.

However, an additional decade and a half of pension underfunding, faulty actuarial assumptions, and extra benefits for workers have driven the system’s unfunded liabilities sky-high.

TRS had only 40 cents of every dollar it needs to pay out future benefits as of August 2015. By any private-sector measure, the fund is already bankrupt.

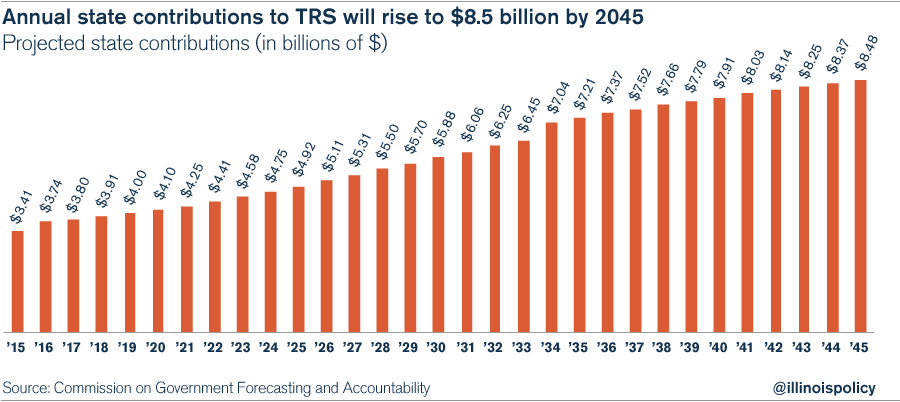

As a result, the state has to contribute more and more taxpayer dollars to keep teacher pensions afloat. According to TRS actuaries, the state will need to contribute over $3.4 billion toward teacher pensions this year alone. By 2030, the state will have to pour $5.9 billion into teacher pensions. By 2045, that amount will rise to $8.5 billion.7

Pension bonds and health care spending

Contributions to TRS are not the only teacher-retirement expense that the state of Illinois pays.

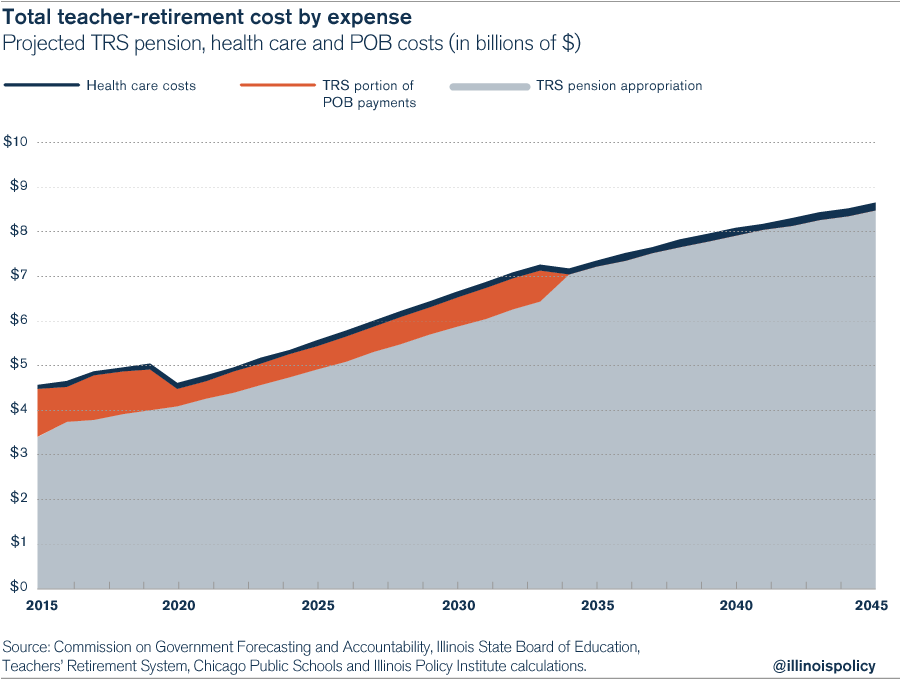

Each year, state government has to make payments on POBs that were approved in 2003, 2010 and 2011 to cover annual pension contributions. In addition, the state has to pay a portion of the costs of health insurance for retired teachers through the Teachers’ Retirement Insurance Program, as well as a portion of the State Employees’ Group Insurance Program.8,9

In 2016, the state will pay $900 million in health care and POB costs combined. That amount will remain relatively steady until 2020, when the end of payments toward the state’s 2011 POB will reduce the combined POB and health care retirement costs.

But by 2025, the combined repayment of the 2003 POB, along with health care and pension contributions, will cause total retirement spending to equal spending on classrooms. Every year thereafter, total retirement spending will surpass classroom spending.

Education spending compromised by Illinois' budget crisis

Unfortunately, the state cannot easily increase education funding to make up for ever-growing teacher-retirement expenditures.

With Illinois’ out-of-control pension crisis, the Illinois Supreme Court’s hostility to pension reforms that include any changes to the future benefits of current workers, and the increasing cost of borrowing due to the state’s lowered credit rating, significant funding increases for Illinois’ classrooms will be few and far between.

Pre-K-12 education won’t be the only budget area taking a hit. Higher-education appropriations will also be crowded out by pensions for educators in the state’s community colleges and state universities. And the federally mandated expansion of Medicaid through ObamaCare will cost Illinois an additional $10 billion between 2014 and 2019.

Our solution

If the current growth in retirement spending continues, Illinois will soon become a state that spends more on teacher-retirement costs than on classroom teaching.

The only way to avoid that outcome is to reduce retirement costs and find ways to spend existing classroom dollars more effectively.

Fortunately for Illinois, there are several innovative ways to do this.

The single most important step Illinois can take to reduce education-retirement costs is to create self-managed retirement plans, or SMPs. SMPs will give both taxpayers and the state more budget certainty and will provide teachers the retirement security they deserve.

The state won’t have to look far for a model SMP: One already exists right here in Illinois. Today, almost 20,000 active and inactive members of the State Universities Retirement System, participate in a 401(k)-style plan. These state-university workers control their own retirement accounts and aren’t part of Illinois’ increasingly insolvent pension system.10,11

Enacting the university-worker plan for newly hired teachers will help stabilize education-retirement expenditures for the state by halting the growth of TRS unfunded liabilities for new teachers. And because only newly hired teachers would participate in any 401(k)-style plans, such a reform would pass constitutional muster. The reform would also make future retirement expenditures easier to estimate, as the cost of SMPs would equal a fixed percentage of TRS’s payroll.

With unfunded liabilities under control, the state would no longer be subject to runaway retirement costs, allowing both the state and local school districts to create more stable budgets.

But bringing education-retirement costs under control is only one-half of education-funding reform. Illinois also needs to embrace educational innovations that will spend classroom dollars more efficiently while fostering an environment that will encourage academic achievement by students.

Enacting a statewide school-choice program would both save the state money and improve educational outcomes for students.

With over half the states in the country, including Wisconsin and Indiana, now offering some form of school-choice program, Illinois can choose from several different successful models.12

For example, just over the border in Milwaukee, Wisconsin, more than 25,000 low-income children receive Choice Scholarships of up to $7,800 to attend the schools their parents select for them – whether religious, private, traditional public or charter. That’s far less than the $13,000 Milwaukee public schools spent per student in 2012.13

Children also perform better academically when they can attend schools chosen by their parents. A recent five-year study of Milwaukee’s program found that more kids are graduating from high school, enrolling in and graduating from four-year colleges, and achieving higher test scores since the start of the program.14

Those same positive financial and academic results have been replicated in numerous states. Several gold-standard studies have found that school-choice programs result in students receiving at least the same, and often a better, education at a reduced cost to the state.15

School-choice programs have been growing rapidly across the country. Nevada, the most recent state to initiate such a program, is offering education savings accounts to almost all of its 385,000 public-school students.16

Illinois would be wise to follow Nevada’s and many other states’ leads.

Another innovation might take the form of new educational techniques such as blended learning, which mixes classroom and personalized digital learning. Not only do such programs often result in higher levels of student achievement, but they can also drive down education costs for the state.

Carpe Diem schools, for example, use individualized online courses of study coupled with live instruction to create a hybrid learning structure that has proved both academically enriching and financially cost-effective.17

Innovations such as school choice and new educational techniques like blended learning could eventually save Illinois hundreds of millions in education costs – freeing up that money for other purposes.