How do you balance a budget when debts are exploding and your population is fleeing?

Due to fiscal crises, both state and local governments are asking more and more from the same taxpayers – encouraging many of them to leave instead.

It’s not easy to balance the budget in a state like Illinois, with crippling debts and a shrinking tax base.

The only way to get the job done is to rein in spending and reform the root of the state’s spending problems: namely the broken pension system and expensive collective bargaining agreements. But Illinois politicians have spurned these measures and haven’t passed a balanced budget since 2001. The state’s debts have been skyrocketing for decades.

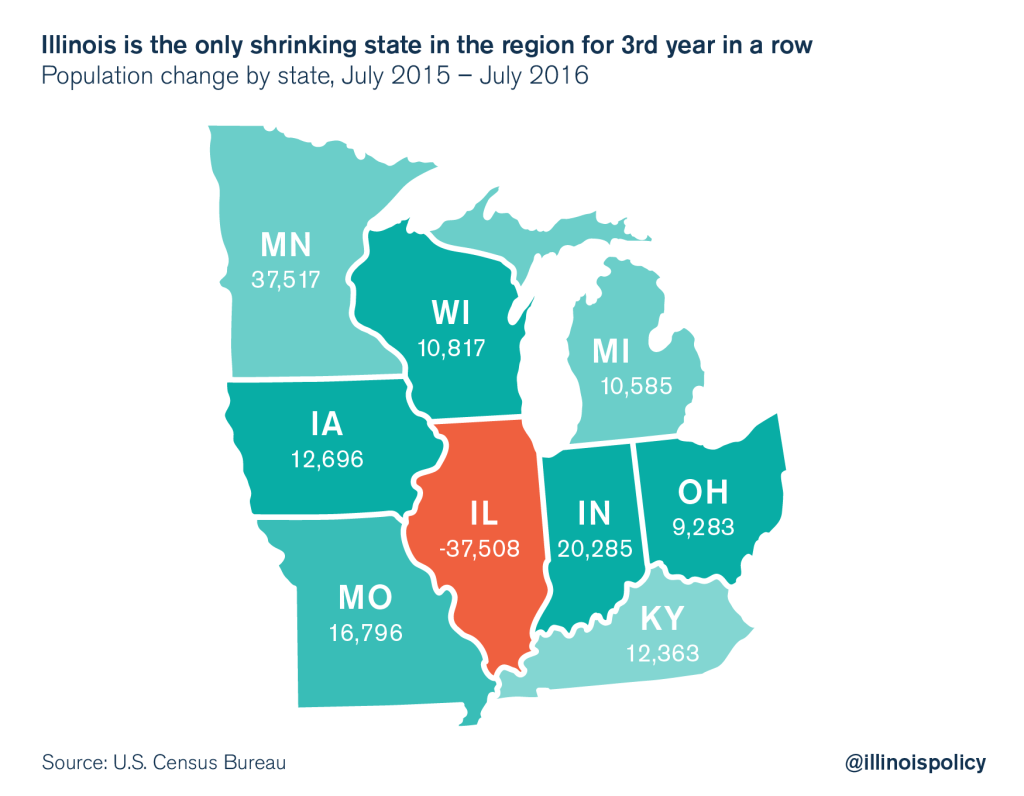

Meanwhile, Illinois – the only shrinking state in the region – has had its population decline for three consecutive years as a result of massive out-migration to other states. In the most recent year of U.S. Census Bureau data, Illinois’ population shrank by 37,500.

Illinois needs more economic growth and more taxpayers chipping in to fund massive, growing debts, but job creation is stagnant and people are fleeing for the nearest border. Yet, despite Illinois being in such an obvious bind, the state legislature has repeatedly proposed massive tax increases on the population.

The logic simply doesn’t make sense. Taxpayers are fleeing, and the state population is shrinking.

If Illinois can’t fund its debt with its current population, how will the state fund its future, larger debt with a presumably smaller population?

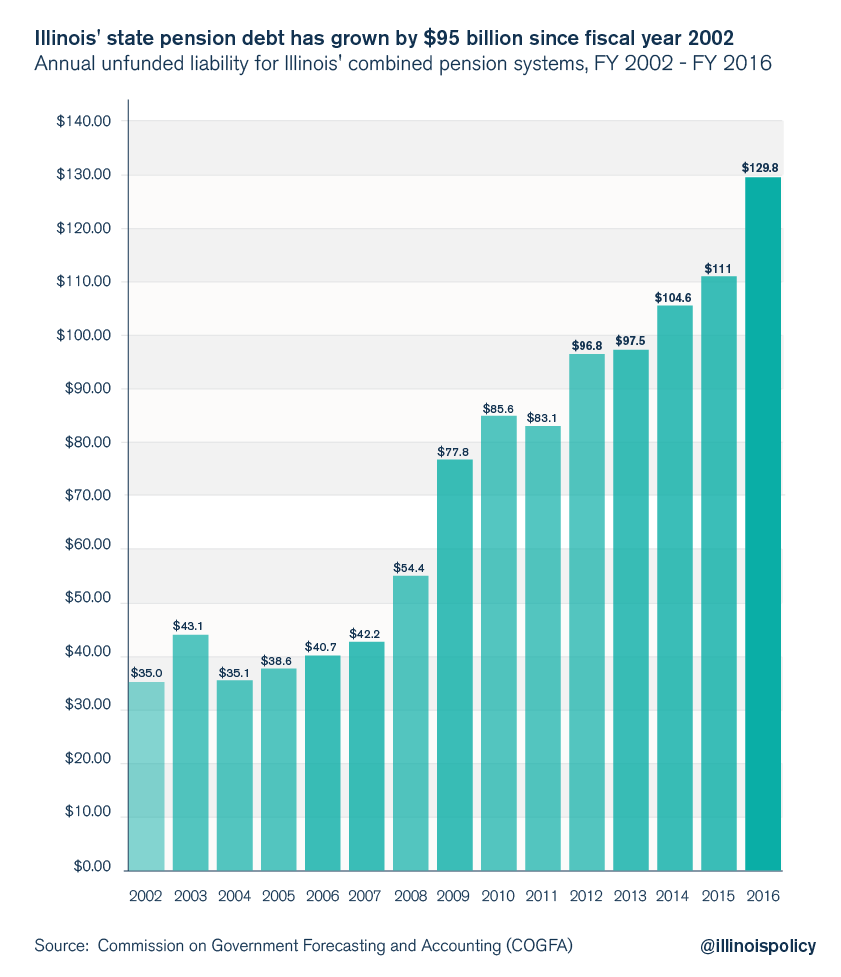

Debts have been exploding across Illinois at both the state and local levels. Consider, for example, pension debt. State pension debts have grown by $95 billion since fiscal year 2002. If Illinois actually budgeted for the pension payments as private sector actuarial rules would require, all of those unbalanced budgets of the past 15 years would look about $6.8 billion worse per year, assuming the additional $95 billion in debt was spread over all years evenly.

The pension debt at the state level is spiraling out of control despite tens of billions in new borrowing and taxes that have poured into pension funds over the last decade.

Local pension debts are also going into a tailspin. And at the end of the day, both state and local governments are trying to extract revenue from the same tax base. Each layer of government is in a race to be first into the taxpayer’s pocket – before the taxpayer flees the state.

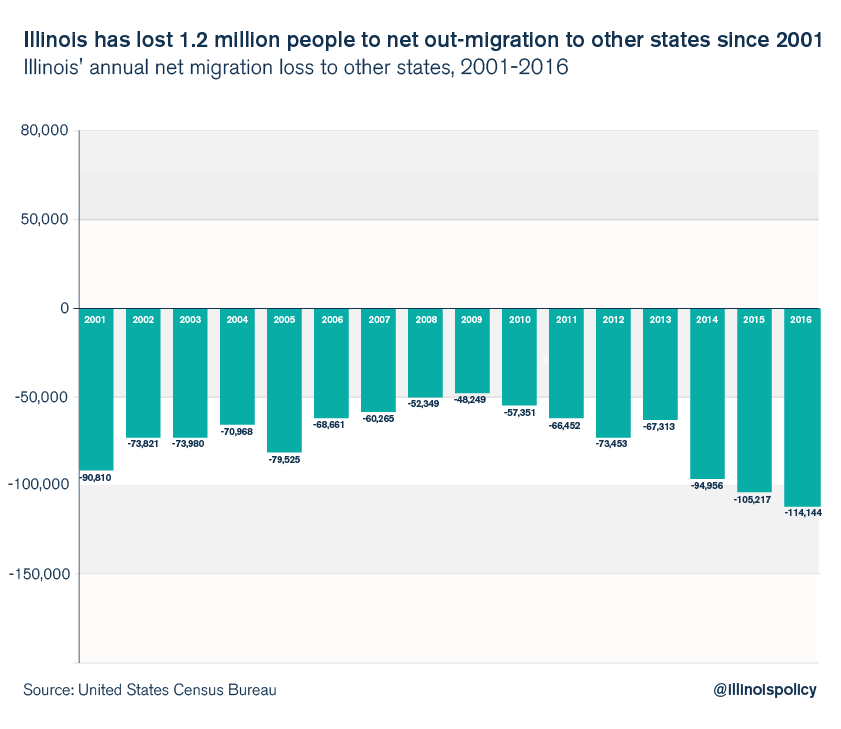

Meanwhile, Illinois has lost 1.2 million people on net through migration to other states since 2001, with record numbers leaving in each of the last three years. Illinois’ total state population has also shrunk three years running, and at an accelerating pace.

Illinois is in trouble. No easy mathematical answers will make these problems go away, and there is a substantial risk that trying to tax the state out of its fiscal mess will catalyze a death spiral. Increasing numbers of people leaving – and their taxable income along with them – will offset revenue from increased tax rates.

Meanwhile, the unfunded pension liability has grown so large and at such a rapid pace that there is a real risk it will spiral out of control, regardless of what taxpayers contribute.

On top of the pension debt are tens of billions in bonded debt, other post employment benefits debt, an expanded, overextended Medicaid system, and costly labor agreements with government unions.

Illinois’ financial crises reach multiple levels of government and are painfully real. The math of financing these debts is becoming less possible as more people leave and the debts spiral out of control. And when it comes to taxing their way out of debts, state and local governments will be targeting the same pocketbooks, putting extraordinary pressure on taxpayers.

Illinois needs to get serious about spending reforms. Collective bargaining laws need to be changed so that state and local governments can save substantially on their work rules and labor costs. The Illinois Constitution needs to be changed to allow for the transition from pensions to retirement accounts workers individually own, which taxpayers can afford.

Illinois is failing to prepare for a future fraught with financial risks. The clock is ticking on the Land of Lincoln as it approaches a financial cliff.