Each year, tens of billions of dollars flow through Illinois state government.1 These flows all depend on methods of payment. In deciding on those payment methods, policymakers must consider a number of important factors, including security controls, cost effectiveness, accessibility, speed and allowance for choice.

This report shows that by adopting best practices across all of these dimensions, Illinois state government can:

- Make payments safer and more accessible for the more than 1 in 5 Illinois households that are unbanked and underbanked

- Improve payment security to better control for vulnerabilities, such as forgery and fraud

- Save at least $1 million a year

There is significant room for improvement in Illinois’ current payment methods, and the state needs a process to keep up with changing payment technologies. For example:

- Illinois state agencies paid out at least $1.3 billion via paper checks in 2018. Paper checks are the most expensive and least secure of the available payment options.

- By statute, a state vendor may receive up to 30 payments per year by paper check.

- Although the Illinois Constitution gives the General Assembly the responsibility to lay out the statutory structure to handle payments, there is little guidance on how agencies can use the most effective payment method for disbursements.

- The state lacks unified standards in evaluating and implementing best practices in payment methods for now and in the future as payment technologies change.

This report outlines a number of important factors to consider in improving Illinois’ payment methods, as well as recommended next steps.

First, government should consider cost and security controls when choosing payment methods. Currently, direct deposit is the most cost-effective method of payment with better security controls, and should be prioritized unless other considerations weigh more heavily.

Second, payment methods should take into account the financial situation of the recipient. Direct deposits are not an option for the 7% of Illinois households that are unbanked. When direct deposit is not an option, the state should prioritize use of debit cards. Debit cards cost the recipient less money to access the funds, are more secure than paper checks or cash, and cost state government less money to administer.

Third, the role government plays is an important consideration when evaluating payment methods. Not all situations are the same, and flexibility is needed. For example, Electronic Benefits Transfer cards are a special kind of a debit card that allows the government to control what may be purchased by the recipient. These EBT cards make the most sense when the government acts as a direct welfare benefactor and wants to make sure the funds are spent consistent with program guidelines.

Fourth, the Illinois General Assembly has the constitutional duty to provide the comptroller, treasurer and state agencies with the statutory structure to handle payments. On the collection side, there is great flexibility in what state agencies may accept as payments. But the disbursement side is more rigid with little guidance.

This report recommends the General Assembly pass legislation that would enable agencies, with approval of the comptroller, to use payment methods that make the most sense under the circumstances. That legislation should also empower the comptroller to empanel an interagency task force to develop guidance on what those best practices are and to update the guidance as payment technologies change. This study gives specific recommendations on the development of a best practice guide by considering the advantages and disadvantages of each payment method, as well as the role of government under each circumstance.

Purpose and methodology

Although advancements in payment technologies have been improving efficiency, saving money and enhancing accountability, state governments have been slow to embrace these innovations.2 In response, several studies have focused on the adoption of new payment technologies by state governments.

In November 2018, the Council of State Governments released its Cash-less State Governments study, depicting how states use electronic payments and debit/credit cards for disbursements and collections.3 Although 32 states responded to its collections survey, only 20 states responded to the disbursements survey.

Illinois was one of the states that responded to both the collections and disbursements surveys. However, the Illinois response was incomplete. Only the Department of Revenue responded, missing the breadth and scope of how Illinois state government uses cashless options in its collection and disbursement activities.

The purpose of this study is to expand on the findings of the Council of State Governments study specific to Illinois, giving a fuller picture of how the government uses payment options and to explore ways Illinois can improve its use of payment methods. Although some of the information revealed in this study came from public documents and literature in the field, most of the data and information were obtained from Freedom of Information Act requests, inquiries and discussions with state officials. The last section of this report catalogs the data by program.

Summary of disbursement data

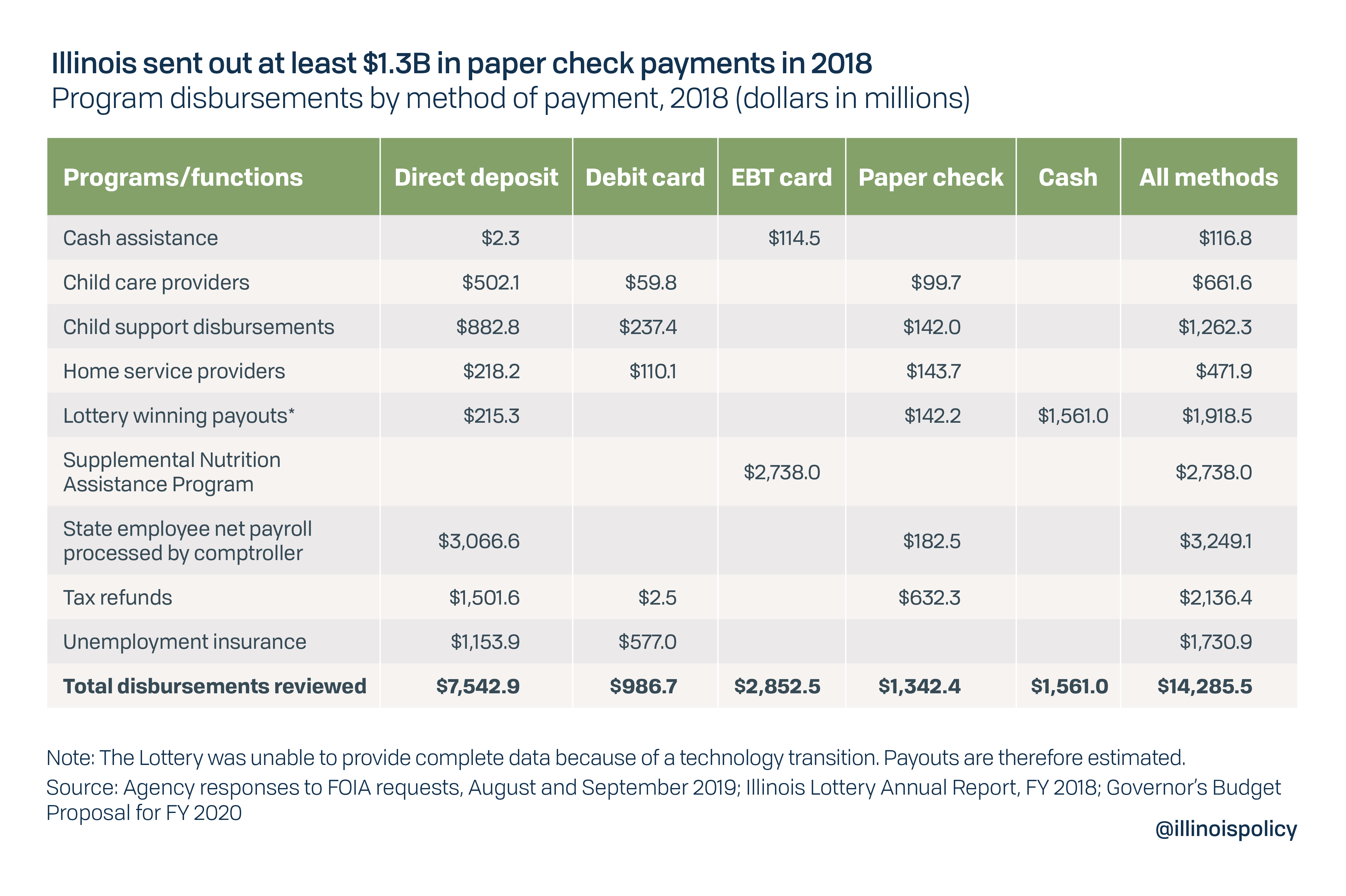

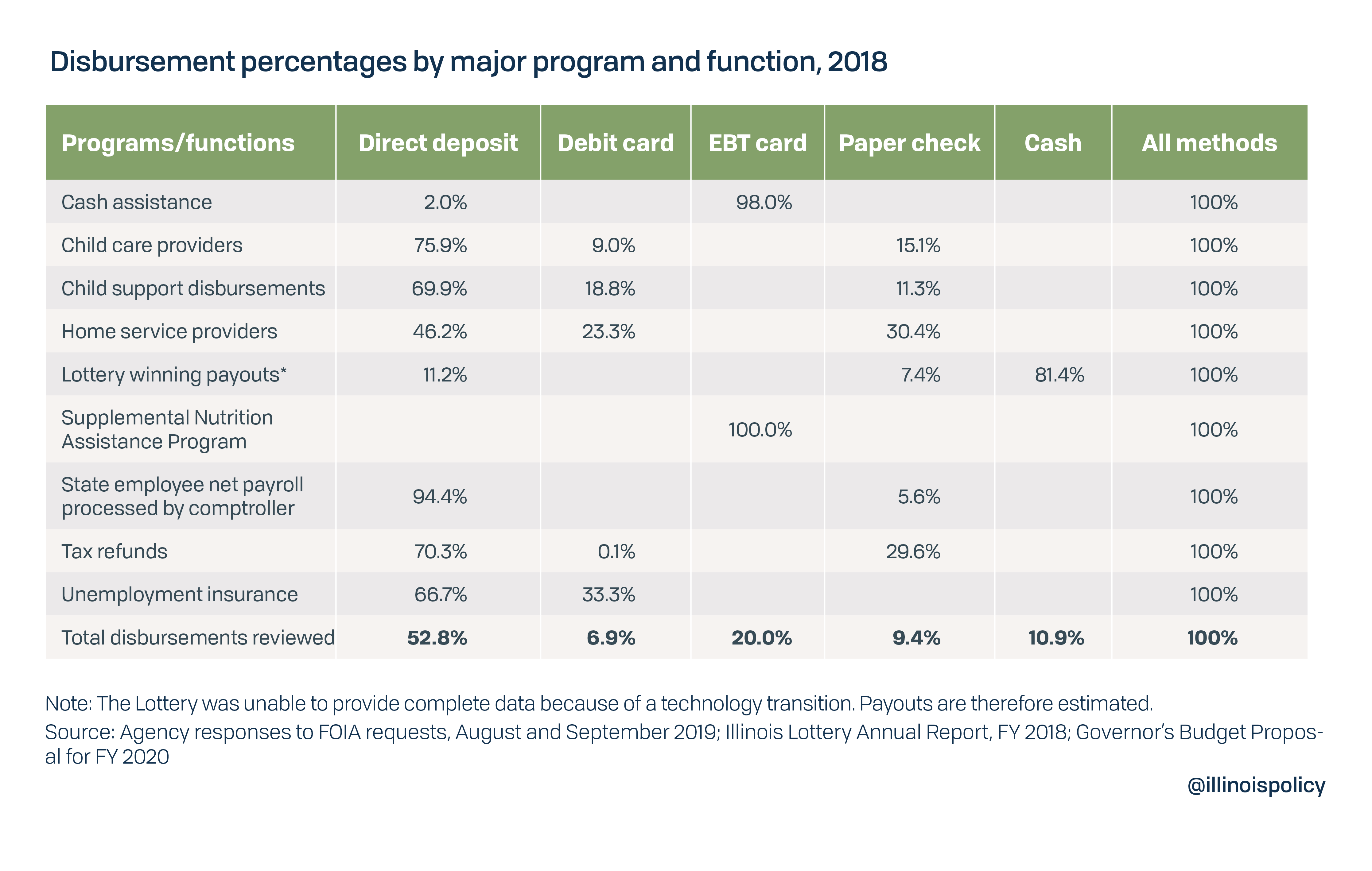

Nine major governmental programs, including basic functions such as payroll, responded to FOIA requests regarding disbursement processes4 totaling $14.3 billion in 2018.

The largest component was $3.2 billion in net payroll processed by the comptroller, followed by $2.7 billion in benefits for the Supplemental Nutrition Assistance Program, also known as food stamps. The next largest function was the refunding of taxes, which totaled $2.1 billion, followed by lottery winning payouts that totaled $1.9 billion.

The data also showed the payment options used varied widely by program or function.

Specifically, in order of magnitude of total payments:

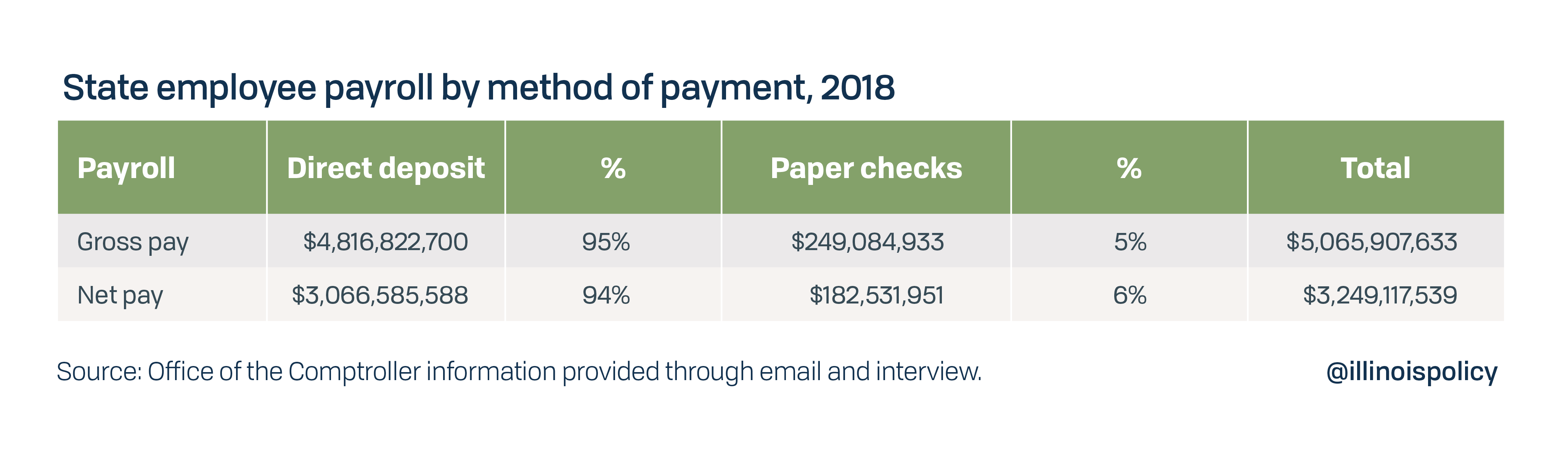

- State employee net payroll payments were mostly direct deposits (94.4%) followed by paper checks (5.6%).

- Food stamp benefits were issued exclusively via EBT cards.

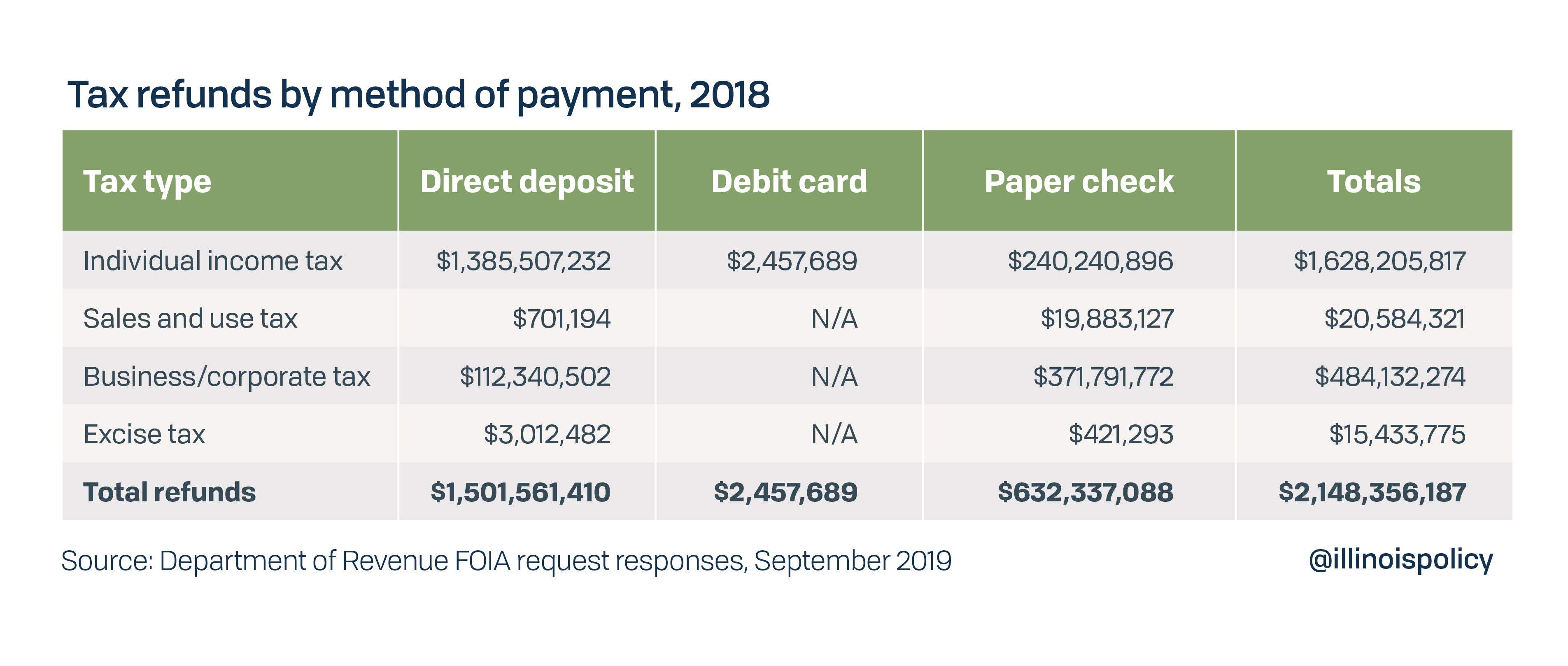

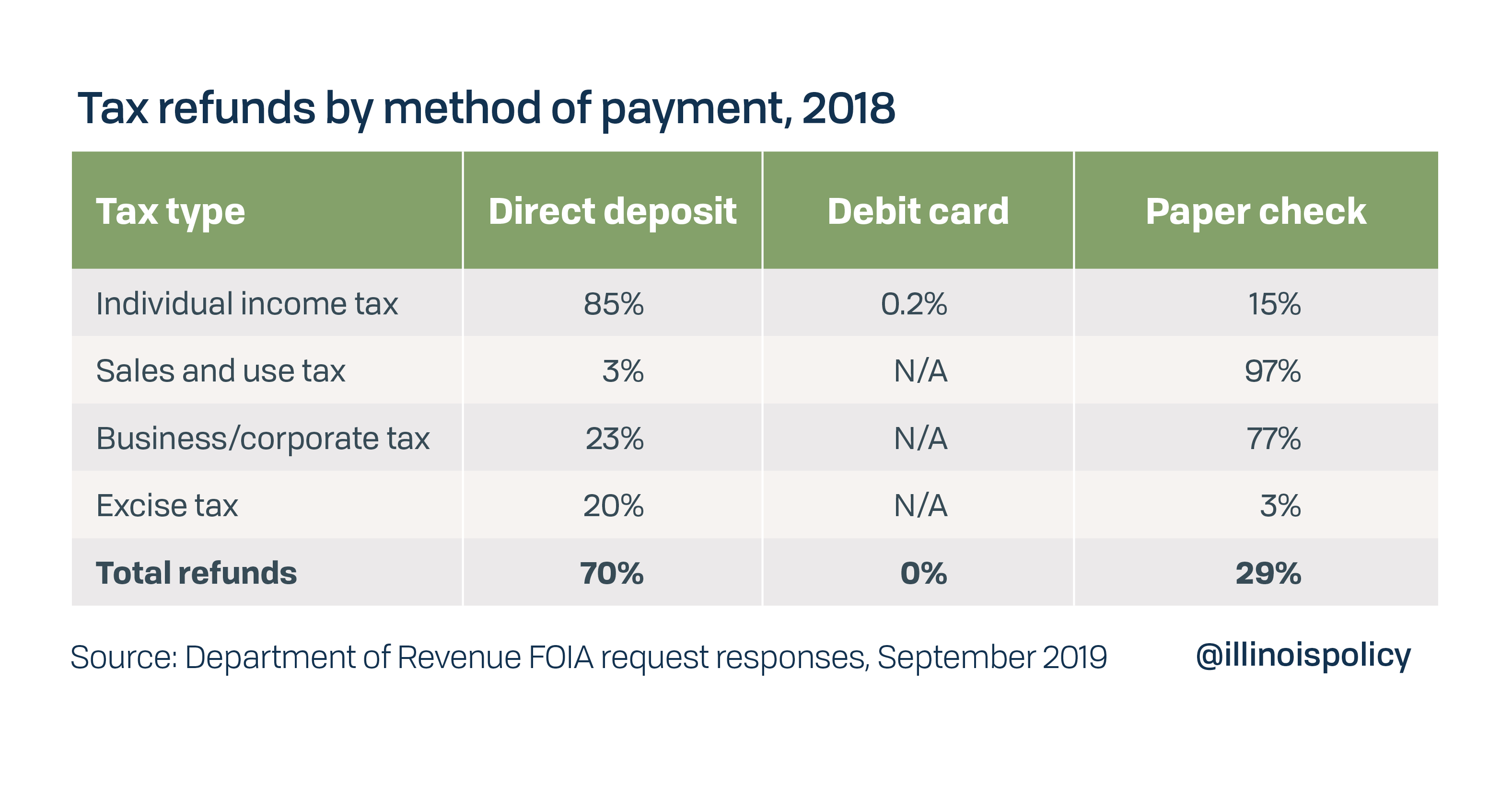

- Tax refunds were issued via direct deposit (70.3%), paper checks (29.6%) and debit cards (0.1%).

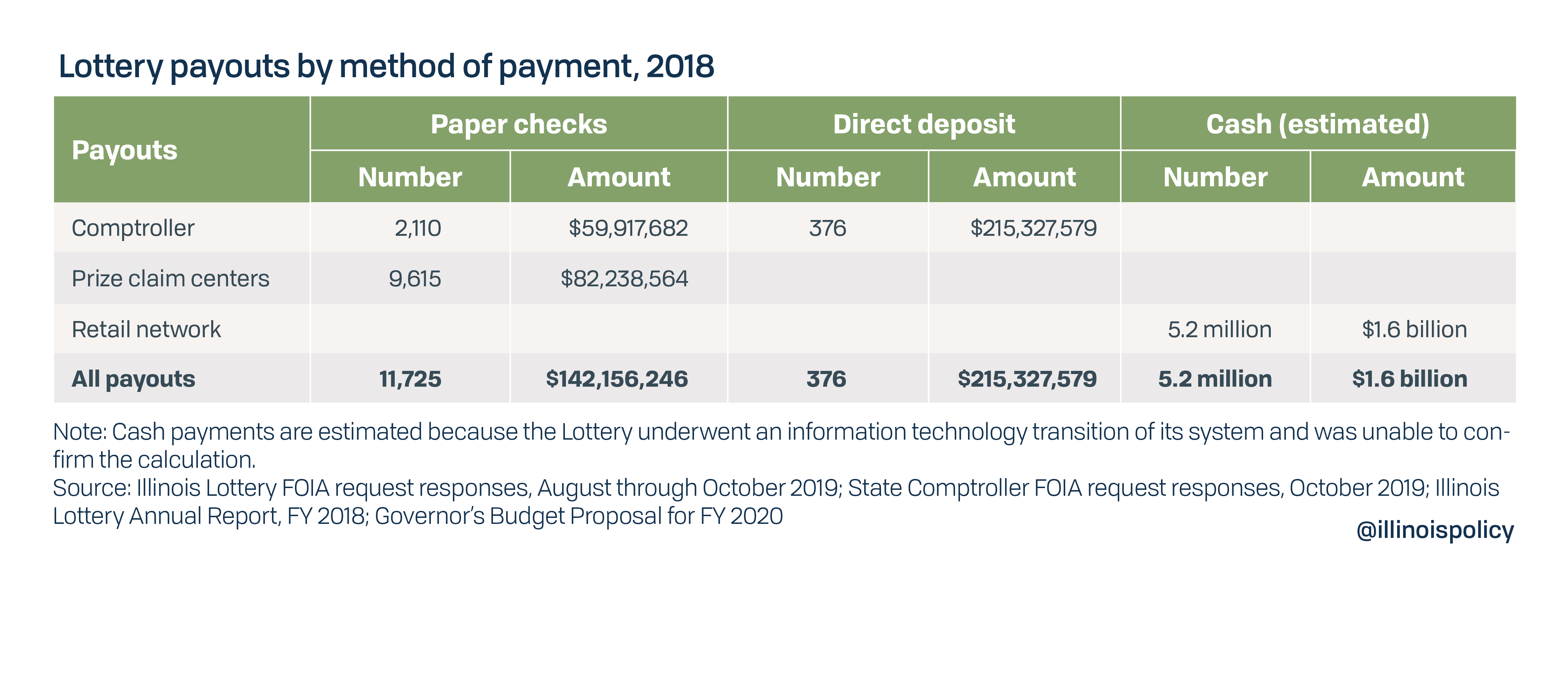

- Lottery winners were paid by direct deposit (11.2%) or paper check (7.4%). The remaining 81.4% of lottery winnings were paid in cash, but these were smaller prizes that were paid through the network of retailers that sell lottery tickets.

- Unemployment insurance benefits came via direct deposit (66.7%) and debit cards (33.3%).

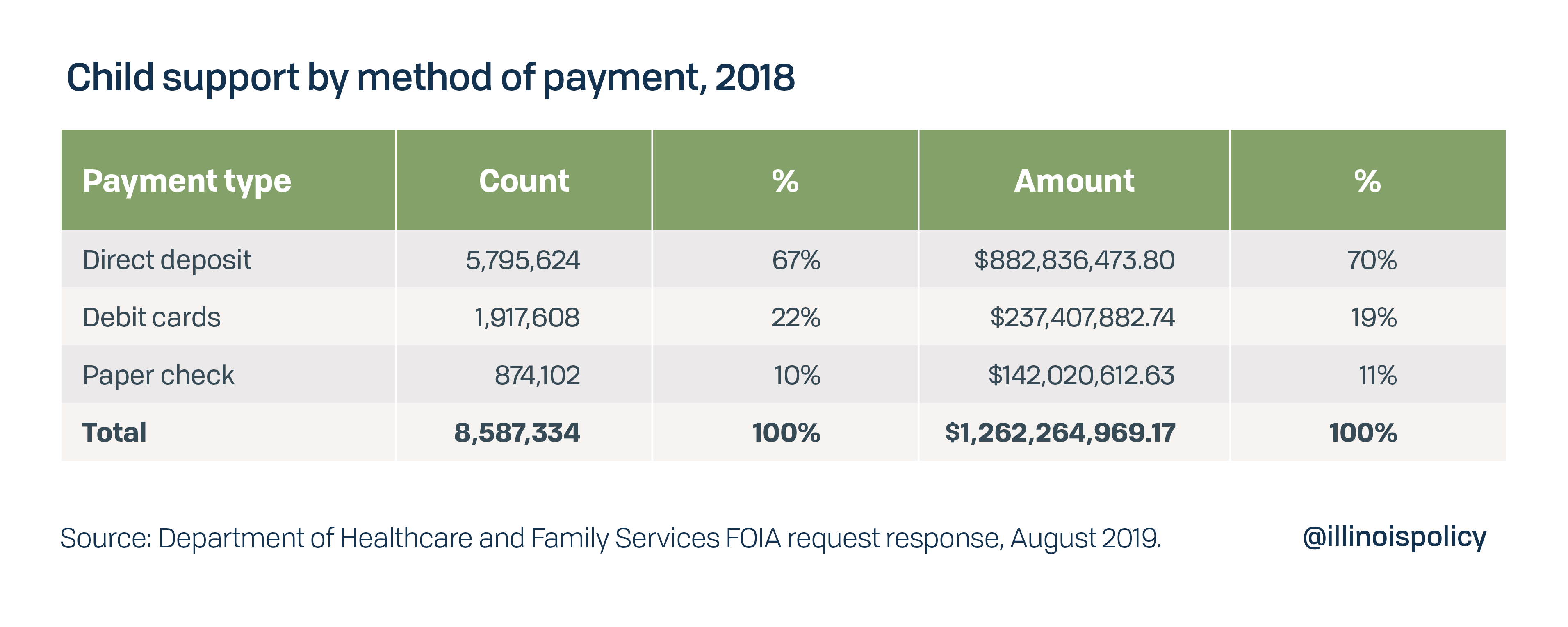

- Child support payment disbursements came via direct deposit (69.9%), debit cards (18.8%) and paper checks (11.3%).

- Child Care Assistance Program providers were paid by a mix of direct deposit (75.9%), paper checks (15.1%) and debit cards (9.0%).

- Home service provider payments broke down similarly but saw almost double the share of payments via paper check, with the following mix: direct deposit (46.2%), paper checks (30.4%) and debit cards (23.3%).

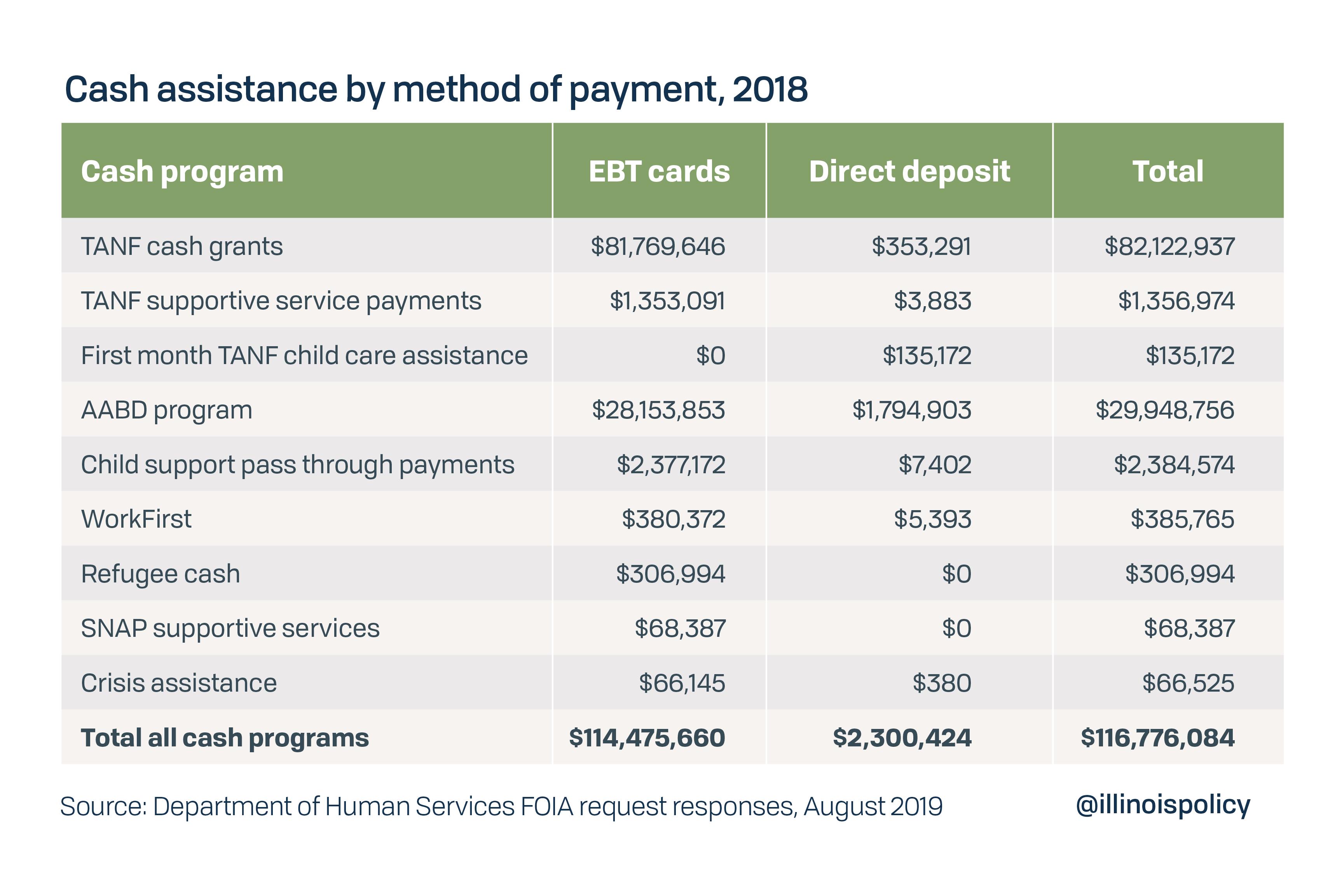

- Cash assistance programs used EBT cards for 98% of its payments and direct deposit for the remaining 2%.

Although there are statutory exceptions, the comptroller is constitutionally responsible for payments of the state. In total, 70% of all payments processed by the comptroller are processed electronically.5

Summary of collections data

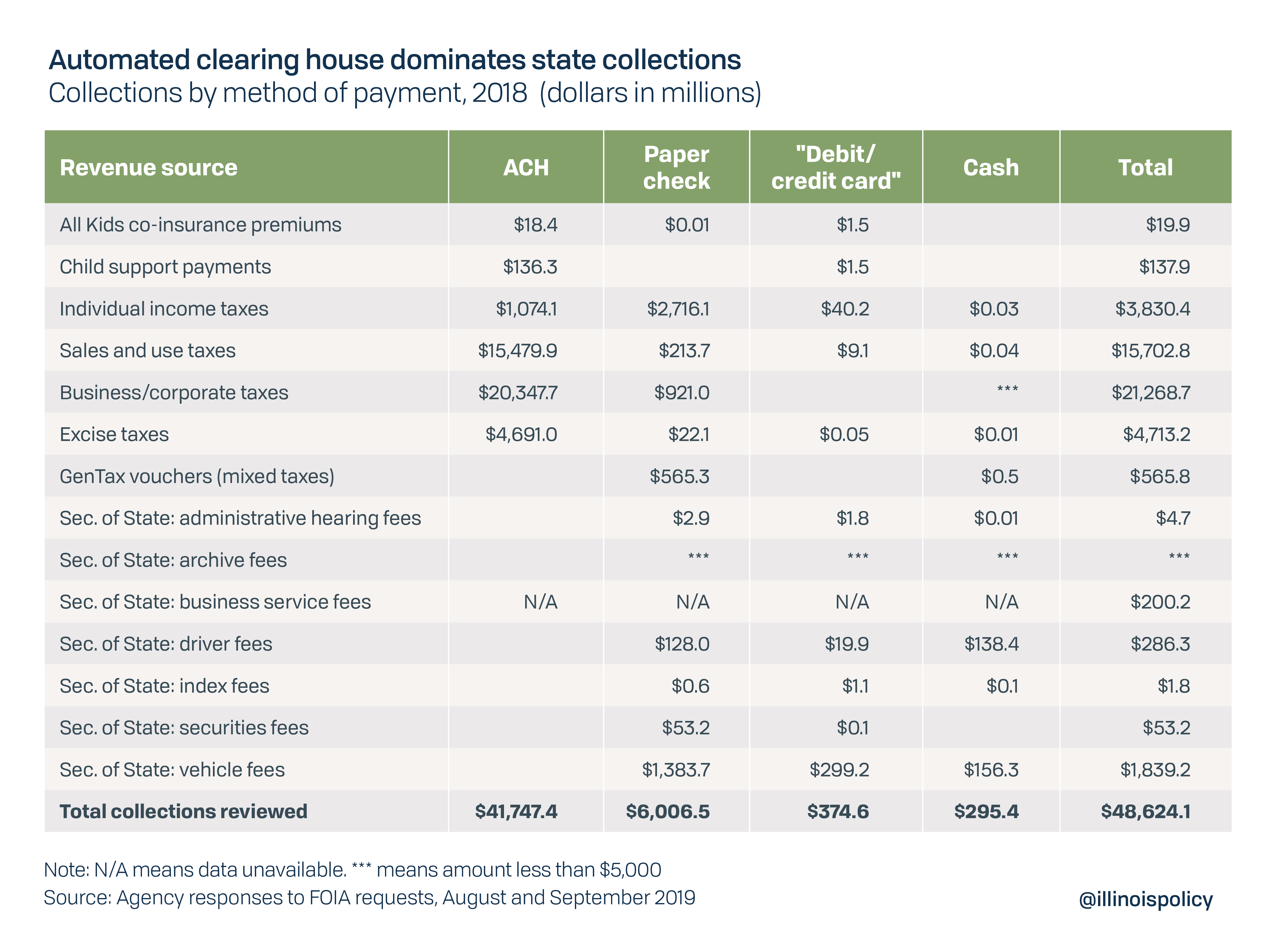

Overwhelmingly, payments collected by the Illinois state government highlighted in this report – accounting for $42 billion in 2018 – come through the automated clearing house, or ACH, a network of all U.S. financial institutions enabling the electronic transfer of funds, including direct deposits. In addition, Illinois collects $6 billion by paper check, $375 million by debit or credit card and $295 million in cash.

For total collections of $48.6 billion in 2018, the following agencies responded to FOIA requests regarding collections for the following programs and functions:

- The Department of Revenue for major categories of tax revenue

- The Office of the Secretary of State for a wide variety of fees

- The Department of Healthcare and Family Services for co-insurance payments received for All Kids (Illinois’ children health insurance program) and child support payments from noncustodial parents

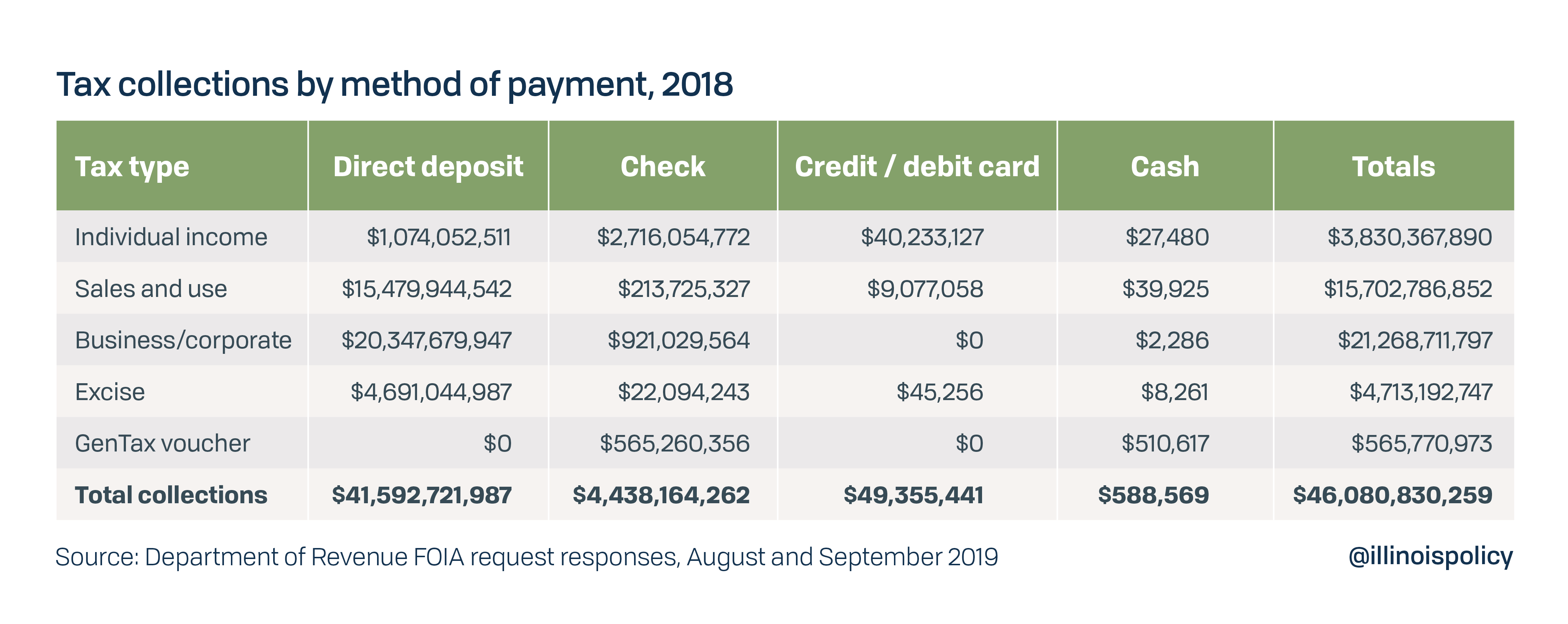

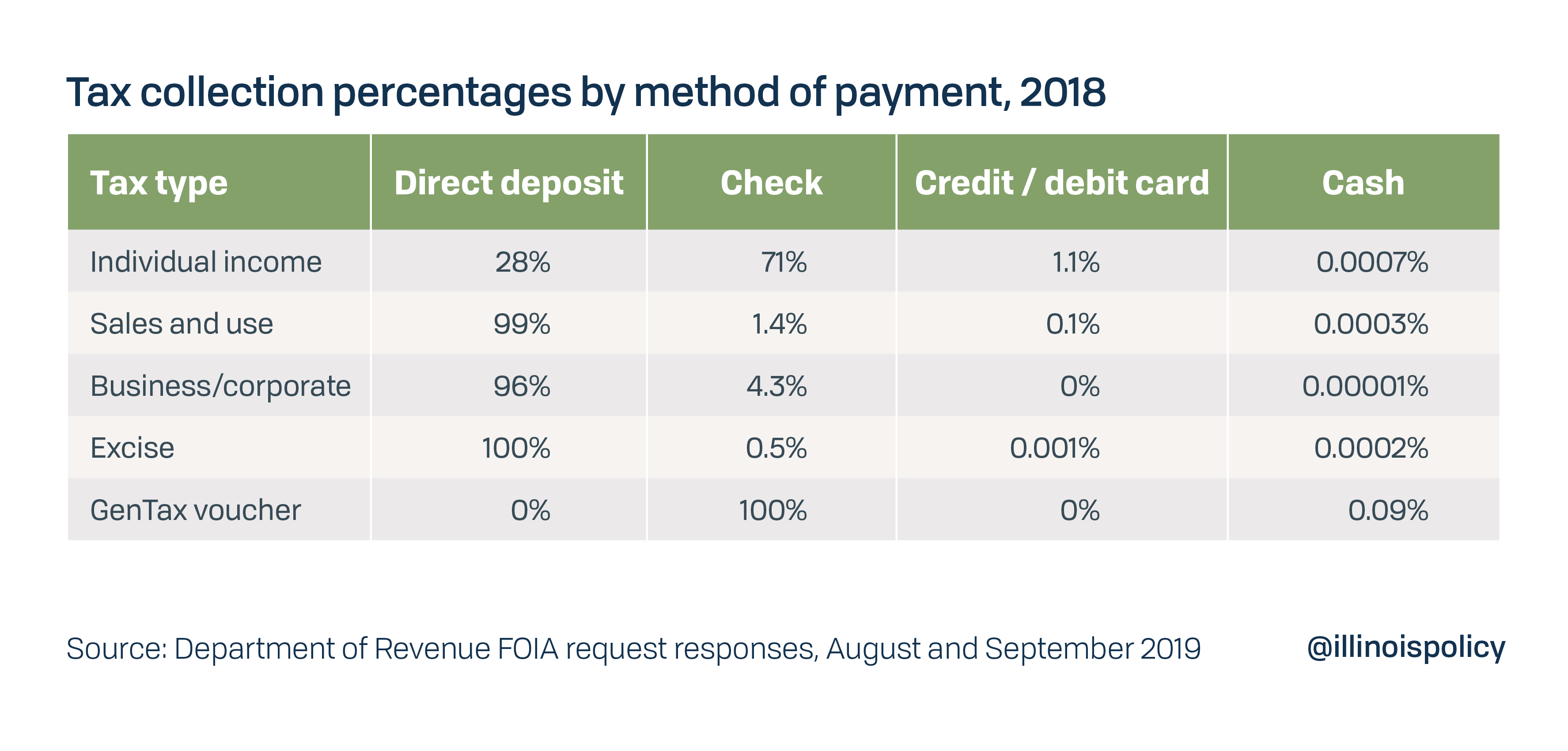

By far, based on the FOIA responses, the Department of Revenue collected most revenue, accounting for $46.1 billion. These collections were composed of:

- Business and corporate taxes ($21.3 billion)

- Sales and use taxes ($15.7 billion)

- Excise taxes ($4.7 billion)

- Individual income taxes ($3.8 billion)

- GenTax vouchers ($566 million)

GenTax vouchers allow taxpayers to submit multiple taxes under one form. Unfortunately, the department was unable to break out the tax components of the GenTax Vouchers.

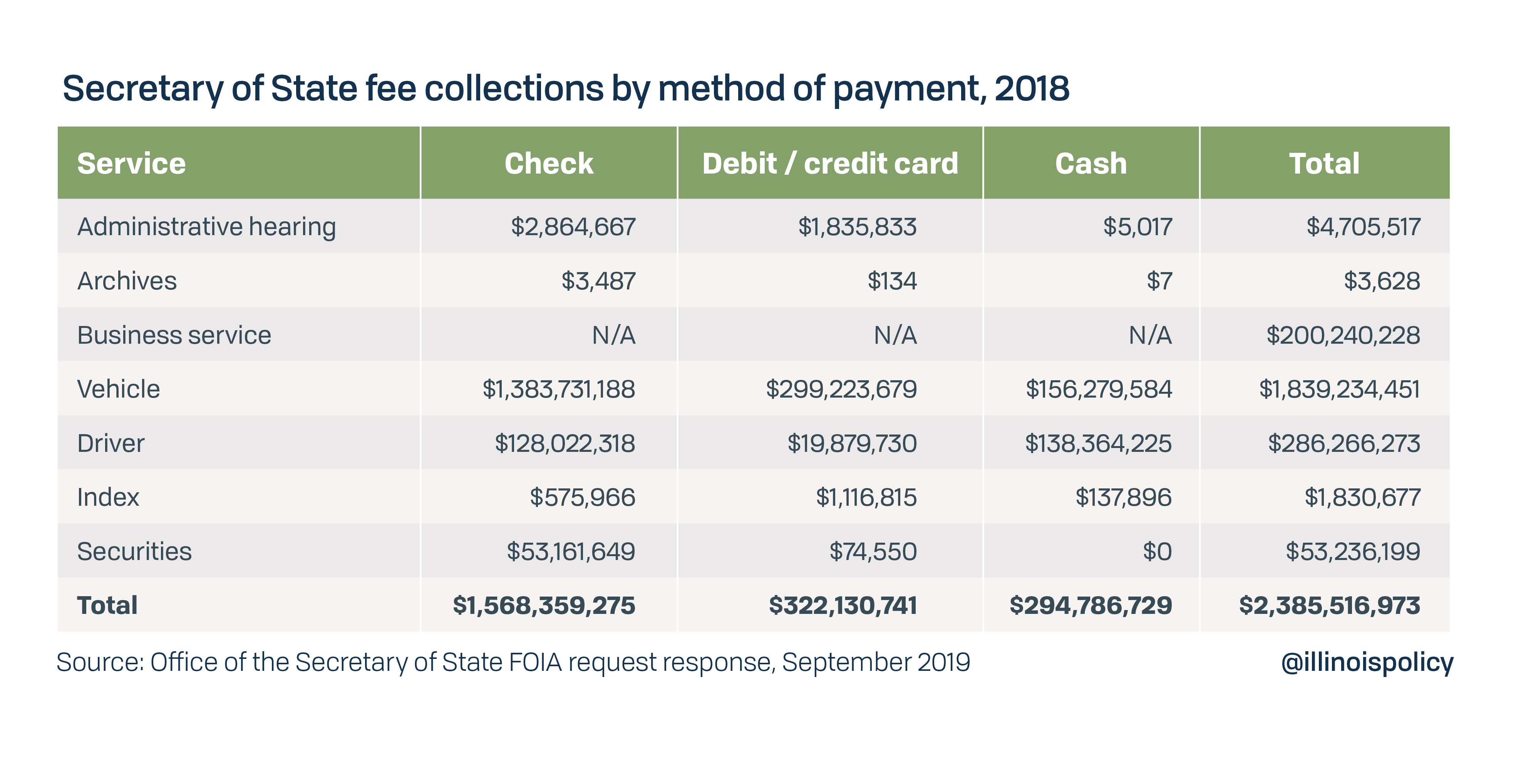

In 2018, the Office of the Secretary of State collected $2.4 billion in fees, composed of:

- Vehicle fees ($1.8 billion)

- Driver fees ($286 million)

- Business service fees ($200 million)

- Securities fees ($53 million)

- Administrative hearing fees ($4.7 million)

- Index fees ($1.8 million)

- Archive fees ($3,628)

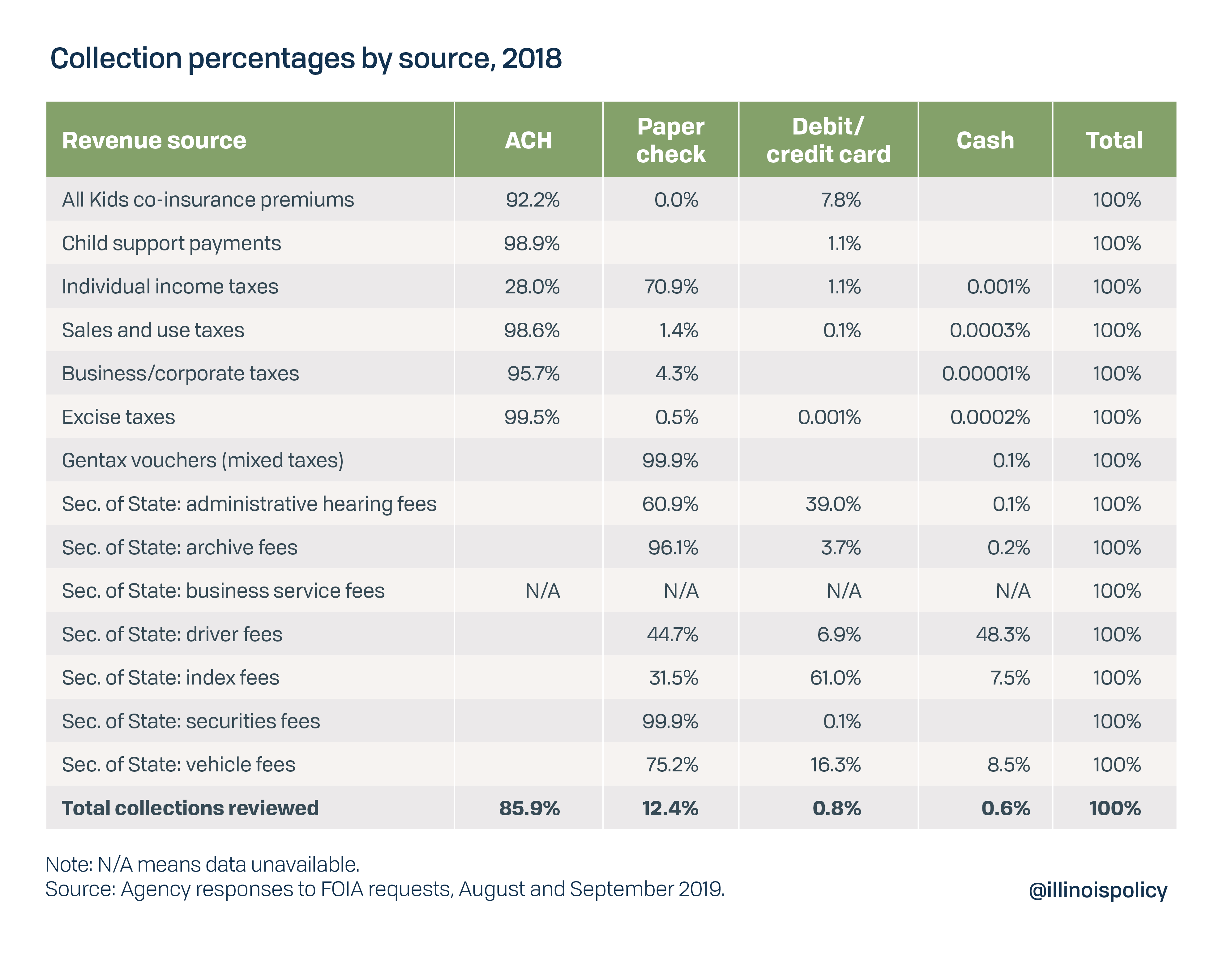

For the Department of Revenue, 90.3% of its collections were paid using ACH. Another 9.6% of the department’s collections were paid by paper check, only 0.1% by debit and credit cards, and 0.001% in cash. Although debit and credit cards were only 0.1% of collections, they accounted for $49.4 million, and cash accounted for $588,569.

Taxes remitted by businesses were predominantly paid through the ACH network, accounting for more than 95% of all collections for business/corporate taxes, sales and use taxes, and excise taxes. Checks accounted for almost all of the remaining collections. In contrast, individual income taxes were paid mostly by paper check (70.9%) with only 28% paid through the ACH network and 1.1% paid by debit or credit cards. Checks also accounted for nearly all GenTax voucher payments.

The Office of Secretary of State collects a wide range of fees, and the payment methods used vary greatly. However, in no case was ACH used. Checks paid for 99.9% of securities fees and 96.1% of archive fees. Debit or credit cards made up all of the remaining securities fees paid (0.1%) and most of the archive fees paid (3.7%), followed by cash (0.2%). Checks accounted for most of vehicle fees paid (75.2%) and administrative hearing fees paid (60.9%), followed by debit and credit cards (16.3% and 39%, respectively) with the remaining amounts paid in cash. Driver fees were paid mostly by cash (48.3%), followed by paper checks (44.7%), and then debit or credit cards (6.9%). Debit and credit cards account for 61% of index fees – which include fees for lobbying registrations, deposit and retrieval of wills and subscriptions to the Illinois Register – followed by paper checks (31.5%), and cash (7.5%). The office was unable to break out business service fees by payment method.

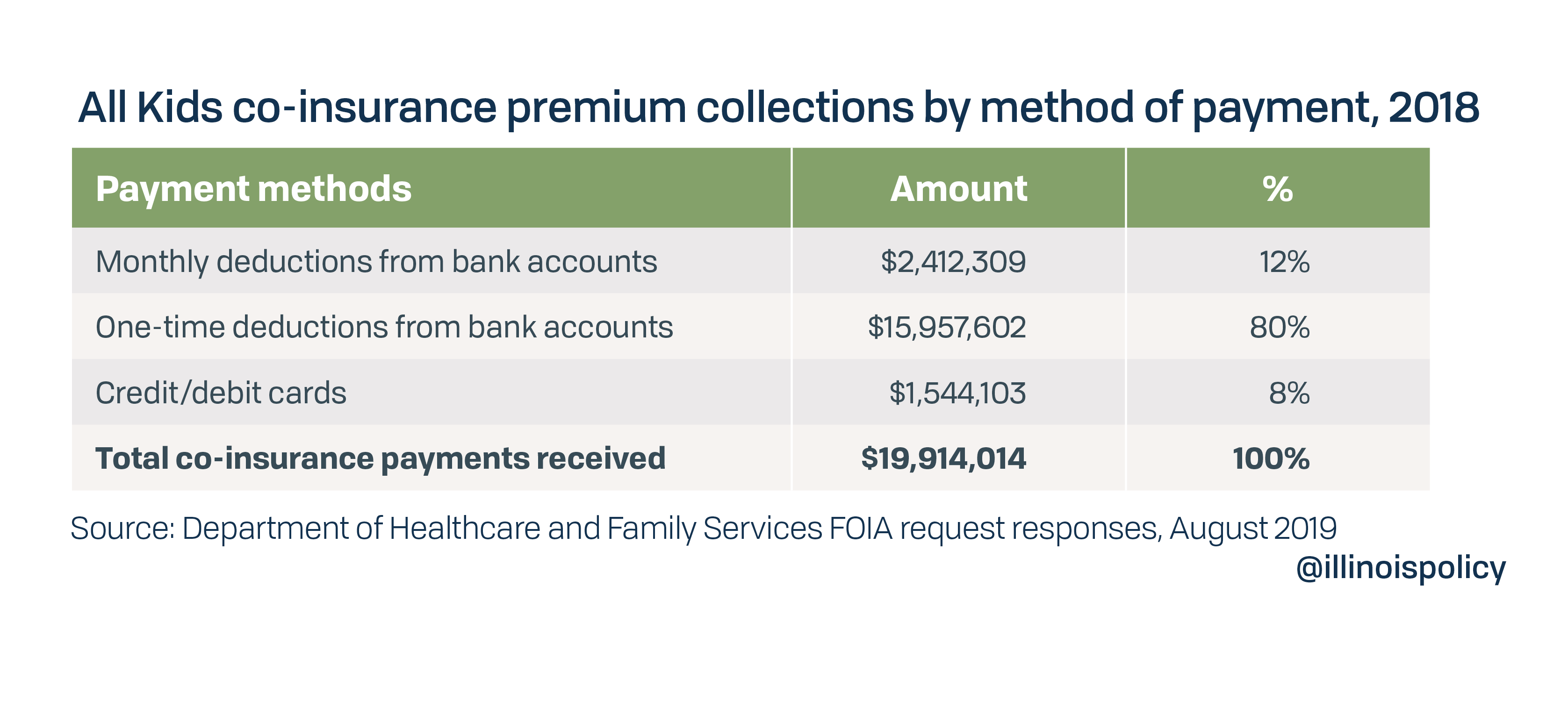

ACH accounted for 92.2% and 98.9% of collected coinsurance premiums and child support payments, respectively, by the Department of Healthcare and Family Services. Debit or credit card payments made up the remaining payments.

Constitutional and statutory guidance

The Illinois Constitution places the duty on the General Assembly to provide the statutory structure for payments and collections by which the comptroller, treasurer and state agencies must operate.

When it comes to accepting payments, state law allows a broad range of payment options that the treasurer can accept. For disbursements, state law is more prescriptive, mandating and allowing for direct deposits in a number of cases, and directing the comptroller to work with the Department of Human Services with welfare assistance payments. Beyond those cases, there is little other guidance.

Considering the continual development in payment methods and technologies, it would make sense for the General Assembly to provide a better structure to guide state officials and agencies for current and future practice.

The comptroller, treasurer, and secretary of state are all constitutional officers elected by the people. The comptroller has the constitutional duty to maintain the fiscal accounts and order payments from funds held by the treasurer. It is the treasurer’s constitutional duty to safekeep the funds until their disbursement upon order of the comptroller. In both cases, the constitution specifies that they shall undertake their duties in accordance with law, placing a duty on the General Assembly to provide the statutory structure enabling the comptroller and treasurer to perform their duties.6

The State Treasurer Act allows the treasurer to accept payments in various forms from “coins, cash, checks, drafts, electronic fund transfers, electronic checks, credit card payments, debit card payments, or other similar payment instruments.”7 This provision gives the administration broad powers in accepting various payment methods.

The statutory guidance for the comptroller is found in the State Comptroller Act.8 In general, all payments must be made by warrant drawn by the comptroller and countersigned by the treasurer. No warrant may be drawn except by an itemized voucher indicating that the expenditure is pursuant to law and authorized.9 However, the statute provides some exceptions to this procedure.10

Moreover, the statute specifically allows the comptroller, with approval of the treasurer, to deposit funds directly into electronic benefits transfer accounts as prescribed by the Department of Human Services, for aid to the aged, blind or disabled, Temporary Assistance for Needy Families, general assistance and child support enforcement services.

The statute stipulates that employee payroll and reimbursement of expenses must be made by direct deposit. If an employee insists on receiving payment by paper checks, the comptroller may charge $2.50 per paper check and deduct the fee from the payment. Likewise, all voluntary deductions from payroll or retirement payments must be by direct deposit, otherwise the comptroller may also charge the entity $2.50 per paper check. The exceptions are employees covered by collective bargaining agreements that do not require direct deposit and employees or vendors who file hardship petitions requesting an exemption.

Furthermore, the statute allows the comptroller to set a threshold, not to be less than 30, of the number of paper checks that a vendor may receive in a fiscal year. The current threshold set by the comptroller is 30. All payments above that threshold must be by direct deposit.

Beyond those guidelines, there is little other statutory guidance for the comptroller or state agencies to determine the best methodologies for making payments.

On the collections side, the two major agencies are the Department of Revenue, responsible for the collection of taxes, and the Secretary of State who has been charged with the collection of a wide range of fees.

The Department of Revenue has been given the ability to allow for electronic fund transfers for the payment of tax liabilities. Non-individual taxpayers with a tax liability over $20,000 and individual taxpayers with a tax liability over $200,000 are required to pay the department by electronic transfer.11

The Secretary of State is constitutionally charged with maintaining the official records of the state. However, the functions of the office have evolved to include the collection of a wide range of fees. In 2018, the Secretary collected $2.4 billion in fees ranging from vehicle fees, driver fees, securities, administrative hearing fees, to business service fees.

Payment method considerations

When deciding on which payment methods for the government to use, there are major issues to consider. These can be lumped into five categories: security controls, cost effectiveness, accessibility, speed and allowance for choice.12 These considerations are important because they provide principles that can help policymakers evaluate different payment methods.

Security controls

Foremost, a payment method must be secure. Private information must be protected to prevent fraud and theft. Online systems must have controls in place to prevent hackers from capturing data and to protect the viability of the transaction. All payment methods have risk, and it is important for government to understand the associated risks.

Cost effectiveness

Each payment method has different costs for both payor and payee. Ideally, the state government should select the most cost effective method for not only itself but should also consider the costs of the other party.

Accessibility

When making payments, the ease of how a recipient can access the funds is important. The issue of accessibility changes depending on the financial circumstances of the recipient. For example, individuals who are unbanked – defined as not having a banking account – or underbanked – defined as using few services from financial institutions, including checking and credit cards13 – have different needs than other individuals who have established accounts with financial institutions. These may include individuals with poor credit history, inconsistent income or employability problems. According to a FDIC survey, 7% of all Illinois households are unbanked, and 15.3% of all Illinois households are underbanked.14

Speed

How quickly payments can be transferred and made available to the recipient is another important consideration. In some cases when payments may be sorely needed but sporadic, such as child support payments, the transactional speed becomes very important.

Allowance for choice

Another consideration is how flexible should the payer be in allowing the payee to choose the type of payment. In some cases, the choices should be limited, but in other cases, presenting more options may be desirable. An example of the former would be a welfare program, such as food stamps, where there are limitations placed on how the recipient may spend the money. In other cases, allowing for more choice may be merited.

Advantages/disadvantages of payment methods

It is important for policymakers to know the basic pros and cons of each payment method given the current state of technology. Among these considerations is the cost. Unfortunately, none of the requests for information from the comptroller’s office and the agencies yielded Illinois-specific cost estimates for the various payment methods. Therefore, this report relies on studies external to the state.

Cash

Cash is legal tender and traditionally acceptable for all transactions. However, its usage in governmental transactions has become practically nonexistent with some important exceptions. In some cases, like the collection of business taxes, the Department of Revenue does not allow for cash for tax liability payments. Overall, cash has been replaced by better methods to transfer money without the obvious risks and difficulties in attempting to transact the exchange using cash.

Paper checks

Paper checks are old technology that allow the transfer of funds from one bank account to another without the inconvenience and risk of carrying bundles of cash. This method requires a supply of paper checks, postage, and an administrative structure for the government to process them. Based on a 2013 study, the Bureau of Fiscal Services of the U.S. Department of Treasury estimated a cost of $1.05 per each issued paper check.15 However, paper checks are not more secure than other payment methods. They can be forged, stolen or lost in the mail. The bank account information is exposed on the paper checks themselves. The incidence of bounced paper checks also adds to the administrative costs of processing the payments. While still widely used and convenient for some banked individuals, businesses and governments, they are inconvenient for the unbanked and underbanked who must sometimes pay exorbitant check cashing fees. Once cashed, the recipient can be vulnerable to theft or robbery without remedy to recover the stolen money.

Direct deposits

A chief advantage of the automated clearing house system of directly depositing money into bank accounts is its cost savings over paper checks. The Bureau of Fiscal Services estimated a cost of $0.09 per each direct deposit, saving the federal government $0.96 per each transaction by not having to write a paper check.16 The cost estimate accounted for not only the postage and price of the paper checks themselves but also the administrative structure necessary to support the operation.

Direct deposits have other advantages over paper checks. The process is more secure than sending paper checks that can be forged, stolen or lost. The transaction is much quicker, allowing the payee earlier access to the money. When the transaction is complete, the money is sitting in the payee’s bank account, enabling the payee to spend the money immediately or to transfer it to a savings or other account.

While ideal for many transactions, especially for clients who are comfortable with online banking and when regular payments can be established, direct deposits are not always the best option. The unbanked cannot use this method simply because they lack a relationship with a financial institution. Other times, when payments are sporadic, such as having to pay a random fee or child support payment on a one-time basis, there are other payment methods that are more convenient than giving bank account information to process a direct payment. Another problem encountered is many governmental entities, especially local governments, do not yet have the capacity or willingness to accept direct deposit. They still prefer paper checks so they can manually control the deposit of the funds, which may need to be transferred into multiple accounts.17

Debit cards for disbursements

Debit cards have been called “a bank account on a card.” They are especially convenient for the unbanked and underbanked. The cards usually carry the Mastercard or Visa logo, allowing the user to spend the money anywhere where Mastercard or Visa is accepted. Payees may withdraw cash, often without penalty within certain parameters, such as with participating merchants. Usually the money is available immediately to the payee, and the cards can be recharged allowing same day access. The cards also allow the banked to transfer the money to their bank accounts, if desired. There are currently fees for this transaction, but the government agency can negotiate the elimination of the fee with the financial institution.

For government payments or disbursement of funds, debit cards can be less costly than direct deposits – often coming at no cost to the government. The financial institution assumes the operational expenses of issuing the cards, working directly with the clients and maintaining the balance of the cards. By contracting out these services, it allows the government agency to reduce staffing and operational costs.

In some cases, governments have negotiated with the financial institutions to share the revenue made by the financial institution in issuing the cards.18 One revenue source is the interest on the card balances, because payees often do not spend the money right away.

Fees, of course, are another source of revenue for financial institutions. Therefore, governments have the responsibility to negotiate with the financial institutions to ensure the fees are reasonable. A review of the terms of the debit cards issued by Illinois agencies for this study and other studies indicate that Illinois agencies have done a fairly good job at keeping the fees reasonable. In many cases, if used properly and within established networks, a payee should have little to no cost associated with receiving payment by debit card. These fees are highlighted in the last section of this report that catalogs payment methods by program.

Debit cards have better security controls over other methods. They eliminate the need to mail multiple paper checks to a payee and require PINs as a safeguard against unauthorized use. Stolen or lost cards can be replaced, and the funds restored.19 As a further benefit, the issuance of cards is federally regulated to safeguard the transactions and protect the consumer, including basic fraud protections from the Consumer Financial Protection Bureau.20

Credit/debit card payments to government

It makes little sense for the government to issue credit cards when making payments. However, the government can accept credit card payments in addition to debit card payments. This is often allowed for the convenience of the payor.

The Illinois treasurer has an ePAY program to help state and local agencies accept electronic payments. The treasurer has contracted out with a vendor that handles the processing of electronic payments, including accepting credit and debit cards. This program can come at little to no cost to the agency as the vendor usually receives convenience fees. Of course, the governmental agency has the ability to negotiate what fees the vendor may charge. The treasurer’s ePAY Program is currently switching vendors from Forte to JetPay.21

EBT cards

Electronic Benefits Transfer cards are a special type of debit card. They use a closed loop system with a pre-approved network of merchants who will accept them. They spend like debit cards, but the types of purchases can be restricted pursuant to governmental program requirements. The best example is the food stamp program. Recipients may only use their food stamp EBT cards to purchase food. Items such as cigarettes or alcohol cannot be purchased with an EBT card.22

EBT cards require a vendor to issue the card. In addition, they require an administrative structure to regulate and work with the network of merchants.

Changing technologies

Cash is rarely used in government transactions, and recent developments in electronic forms of payment are making paper checks obsolete.23 The technologies continue to evolve with virtual cards, near-field communications, mobile wallets and digital currency. It is not yet clear which of these technologies will take hold or what future ones will emerge, but it is important for government to keep up with the changes to serve its citizens better with more consumer convenience, improved cost effectiveness, and enhanced security controls.

Governmental roles

For policymakers to decide which payment methods are most appropriate to use, it is not enough to consider only the advantages and disadvantages of each method. The role played by government specific to the program or function is also a major consideration. These roles can drastically change the circumstances for what payment methods should be used and promoted. The following categories provide an analytical structure to help understand the governmental roles of government when it comes to disbursements and collections.

Disbursement roles

Tax collections refunder

Governments obtain most of their revenue through taxation. Constitutional protection guarantees that taxation must be uniform and cannot be capricious and arbitrary. Therefore, governments are constitutionally obligated to refund tax overpayments. The Department of Revenue regularly refunds tax overpayments. Governments are also not entitled to overpayments of fees and fines and are legally obligated to refund those overpayments as well.

Lottery winnings cashier

Governments also gain revenue by operating lotteries. The revenue is not based on legal forced confiscation of property as with taxation but premised on enticing people to voluntarily part with their money to purchase chances to win money. By operating the lottery, government then becomes obligated to operate as the cashier, paying the winners of the lottery games.

Employer

Government is a very large employer and provides not only wage and salary payments directly to employees but also all the other payroll costs, benefits and reimbursement of expenses.

Procurer

Government needs capital resources, such as facilities, equipment and tools, in order to deliver its services.

Contracting-out service provider

Many government services are contracted out to private providers. Examples include contracting out to engineering and construction firms to build or reconstruct highways.

Direct welfare benefactor

When government pays welfare benefits directly to recipients, it plays the role of direct welfare benefactor. Sometimes the welfare programs have restrictions on how the money may be spent, which is an important consideration, and other times there are no restrictions. Examples include food stamps, cash assistance and refundable tax credits.

Indirect welfare benefactor

Often welfare benefits are paid to a third-party provider who provides services to the welfare recipients. The money never passes through the recipient. In these cases, the government is an indirect welfare benefactor. Examples include Medicaid, All Kids, Child Care Assistance Program services, and Section 8 housing vouchers.

Intermediary payment facilitator

Other times, the government acts as an intermediary payment facilitator by collecting from the payor and then providing the payment to the payee. The child support enforcement program is an example.

Collection roles

Tax collector

Taxation is the major means by which government receives its revenue to operate. Although the line between taxes and fees has been blurred and is often confused or used interchangeably, it is still helpful to make a distinction. Technically, taxation is the taking of property for the purpose of providing general revenue for government to operate that are not attached to a specific service. In contrast, fees are charges that cover the costs for delivering a specific service, such as issuing a license. The lines can become blurred because some taxes are inappropriately called fees. Other times, fees are in excess of their costs to provide the specific service. Examples of taxes are many, including real estate transfer taxes, individual income taxes, excise taxes and sales and use taxes.

Fee collector

Government also collects fees that should theoretically cover only the cost of providing a specific service. See the explanation under tax collector for more detail.

Fine collector

Government collects fines imposed on individuals for infractions of the law.

Cost sharing payment collector

Some welfare programs require recipients to share in the cost, and government can collect cost sharing payments. For example, the All Kids program, which is Illinois’ children’s health insurance program, includes coinsurance payments for qualifying families in the upper two income tiers of the program. These payments are collected directly by the Department of Healthcare and Family Services.

Intermediary payment facilitator

Government also acts as an intermediary payment facilitator by collecting payments from one party and disbursing the funds to another party. This role has already been described.

Conclusion

In many ways, state government payment methods in Illinois are currently reasonable. More than 70% of all payments issued by the comptroller are electronic. EBT cards are used for food stamps and cash assistance. Employee payroll uses direct deposit most of the time, and the comptroller may charge $2.50 for each paper check it issues. Debit cards are available for child care providers, home service providers, child support payments to custodial parents, tax refunds and unemployment insurance.

However, there is still much room for improvement.

Responses to Freedom of Information Act requests show $1.3 billion in disbursements were issued by paper check in 2018. In addition, data on billions of other paper check transactions issued by the comptroller were not captured by this study. Allowing those payments to be made electronically through direct deposit or through debit cards would be beneficial on several levels:

- It would help disadvantaged Illinoisans with their personal finances, specifically the 22.3% of the households who are unbanked or underbanked. These households would have better accessibility with lower costs.

- It will save state government money. Although the data collected by the comptroller’s office does not allow for a precise estimate, savings should easily exceed $1 million.24

- Security controls would be enhanced, ensuring taxpayer money is being spent appropriately.

In addition, there is potential for the Illinois Lottery to reduce its costs, enabling it to transfer more money to the state. Most payouts are in cash or by paper check, and these are mostly for the smaller prizes. There is no reason to doubt that a significant percentage of these winners will be unbanked or underbanked. Therefore, the Lottery should explore ways to limit payouts by paper check, making use of debit cards and direct deposits instead.

The General Assembly has provided statutory authority to collect a wide array of payments, providing agencies flexibility on the forms of payment they collect. Overwhelmingly, the automated clearing house is the most popular choice.

There is statutory authority specific to the forms of payments the comptroller may use, such as direct deposit for payroll and vendors and EBT cards for Department of Human Service programs. However, there is little room for allowing alternative methods when they may be justified and when technologies change.

Recommendations

General recommendation

The Illinois General Assembly has the duty to provide the statutory structure for payments and collections for constitutional officers – the treasurer, comptroller and secretary of state – as well as other state agencies in performing their duties. Given the current technologies used, the best payment methods depend on the specific role played by government as well as the strengths and weaknesses inherent in the payment methods themselves. Furthermore, the technologies are changing. What are understood to be the best methods today may change as technologies evolve and new methods are introduced.

Therefore, it is recommended that the General Assembly pass legislation that gives agencies the flexibility to adopt those payment methods best suited for their purposes, provided that the methods are approved by the comptroller. This flexibility will allow the agencies to adopt best practices without the need for further legislation and to change practices as payment method technologies evolve. Current restrictions in the law, such as the threshold of allowing 30 paper checks for vendors, should be repealed.25

Furthermore, the legislation should empower the comptroller to empanel an interagency task force for developing guidance on the best practice of payment methods. The comptroller shall chair the task force and the treasurer shall be the co-chair. Other members may include large agencies and private sector experts. The task force shall meet periodically to update the recommendations as payment methods evolve over time.

Recommended analytical structure for agency guidance

Given greater flexibility, the following analytical structure can be used to develop guidelines on best practices in payment methods.

Direct welfare benefactor

When government plays the role as direct welfare benefactor, it is necessary to decide if there should be restrictions on how the recipient may spend the money. Most often, if not always, these restrictions need to be in place. If this is the case, then EBT cards are the best option and, in fact, ought to be the only option. EBT cards operate like debit cards, except on a closed system where the vendors agree to participate. This closed system enables the governmental agency, such as the Department of Human Services, to impose restrictions on what can be purchased. A good example is the food stamp program that restricts purchases to food items.

In cases where there is no need for program restrictions on what recipients may purchase, which assumes a level of trust of the recipients, the payments should be either debit cards or direct deposit based on the financial circumstances and preferences of the recipients. If the recipient of the aid is unbanked, the logical choice is debit cards. If the recipient is banked or underbanked, then direct deposit is likely the best option. In no case should the payment be made by paper check, unless it can be demonstrated that the other two options are infeasible.

Indirect welfare benefactor

When government functions as the indirect welfare benefactor and the provider is banked or underbanked, such as Medicaid and All Kids providers, then the best payment option should be made using direct deposit. However, the State Comptroller Act allows a vendor to receive up to 30 payments annually by paper check. It would be more cost effective if this provision were repealed.

When government is the indirect welfare benefactor and the provider isunbanked, such as with many child care assistance program providers or home service personal assistants, then the best option is currently the debit card. In these cases, the agency implementing the program may consider providing advice to the providers to help them understand the advantages of becoming banked.

Intermediary payments facilitator

When government is the intermediary payments facilitator, such as with the child support enforcement system, the agency should allow the payers, e.g., the noncustodial parents, to pay in a manner that encourages payment. In this case, the important public policy goal is that the custodial parent receives payments to help with child rearing expenses. Setting up a direct deposit system, or even involuntarily garnishing wages, may be the simplest method to guarantee payments. However, there will be some situations where this will be infeasible because of employment difficulties and infrequency of income. In those cases, the ease of payments becomes critical. If the payer chooses a more convenient way of making payments that has a cost associated with it, such as paying by credit or debit card, then it is reasonable to charge the payer a convenience fee to cover the additional cost.

Payments to the payee, e.g., the custodial parent, should be by direct deposit or debit card, depending on financial circumstances. If the payee is banked or underbanked, then direct deposit currently makes the most sense. If unbanked, then debit cards are currently the best option. Paper checks should not be used, unless it can be demonstrated that the direct deposit or debit card methods are infeasible.

Contracting out service provider

When the government contracts out services, the government has the ability to set the terms of payment. In these cases, direct deposit should be the default option. It is unlikely that the contractor would be unbanked, but if it is, and this fact does not raise other concerns such as reliability of the service, then debit cards would be the best option. If the vendor insists on receiving payment by paper check, then the current policy of charging $2.50 per check is reasonable.

Employer

Current Illinois policy for paying its employees makes sense. State employee payroll and reimbursement of expenses are paid using direct deposit. Employees are charged $2.50 for electing to have their paycheck or expense reimbursement by paper check, unless the employee can demonstrate hardship. Because some low-paid employees may be unbanked or underbanked, debit cards should also be offered as an option, which will require amending state law.

Procurer

When government procures supplies, it should rely on direct deposit and debit cards. On rare occasions paper checks may be necessary when the first two methods are infeasible.

Tax/fee collections refunder

When the government refunds overpayment of taxes, or rare overpayment of fees, the options should be direct deposit, debit cards and paper check, in that order. Taxpayers that are banked or underbanked should opt for direct deposit. If they are unbanked, then the best option is debit cards. Check should be the last option but still made available.

Refunding overpayment of taxes differs from the other situations considered. The overpayment belongs to the taxpayer. It is not the property of the state, nor was it at any time the property of the state. By contrast, other programs disburse funds that were lawfully received through taxation, fees and other revenue. For example, cash assistance is state revenue lawfully received being appropriated for a government program that provides help to individuals. Therefore, in the case of taxation, the taxpayer has a right to specify his or her preference for the payment and should not be charged a fee if the taxpayer prefers to be paid by paper check. Nevertheless, the state can influence the decision by making payment by direct deposit or by debit card the default method and notifying taxpayers of the advantages of those payment methods.

Lottery winnings cashier

When paying out large lottery winnings, currently defined as over $25,000, the current government policy is payment by either paper check or direct deposit, which is paid by the comptroller. The default payment should be direct deposit. If someone is unbanked, then they should be encouraged to use the paper check to open a bank account. For midrange winnings, now defined as between $600 and $25,000, the payments are made only by paper check by the Prize Claim Centers. The Lottery should consider in these circumstances to also allow for direct deposit and debit cards, making paper checks only available when requested.

For winnings less than $600, the prizes are mostly cashed in at the participating retailers. However, the volume of these small prize winners is very large, with over 5 million winners in 2018. The Lottery should explore the possibility of using debit cards that could raise additional revenue for the state, which is its primary purpose.

Appendix: Catalog of disbursements by major program

Program: Cash assistance

Type: Government to person payment, or G2P

Agency: Department of Human Services

Description: Combination of programs administered by the department to provide cash assistance payments to individuals

Cash assistance includes the following programs

- Temporary Assistance for Needy Families (TANF) program

- TANF supportive service payments

- First month TANF child care assistance

- Aid to the Aged, Blind and Disabled (AABD) program

- Child support pass through payment

- WorkFirst

- Refugee cash

- SNAP supportive services

- Crisis assistance

Payment options

- EBT card (Illinois Link Card)

- May be combined with SNAP Link Card

- Direct deposit, if requested by client

Volume of payments (2018)

Costs/fees/surcharges

- Client EBT card costs

- No charge for using Link Card at point-of-service terminals

- Clients are allowed two free withdrawals at ATMs per calendar month. Thereafter, there is a $1 transaction fee.

- Clients are allowed two free balance inquiries at ATMs per calendar month. Thereafter, there is a $0.50 transaction fee.

- No bank surcharges allowed on any Link transaction

- Annual cost of contract: $7,797,000 (Contract: #981AQ164000)26

Utilization of third party vendors

- Conduent, Inc., per Link III comprehensive contract

Program: Child Care Assistance Program (CCAP) providers

Type: G2P

Agency: Department of Human Services

Description: CCAP provides low-income, working families with access to affordable, quality child care services in licensed centers or unlicensed home-based settings. State payments are made directly to the providers.

Payment recipients

- Licensed child care providers

- License-exempt home child care providers

Payment options

- Direct deposit

- Paper check

- Illinois Debit MasterCard by Comerica Bank27

Volume of payments (2018)28

- Direct deposit: $502,140,285.14 (76%)

- Paper check: $99,687,180.15 (15%)

- Debit card: $59,787,453.36 (9%)

Costs/fees/surcharges

- Recipient costs for receiving payments by debit card

- Recipients are encouraged to use ATM locations with certain brands (Charter One, Privileged Status, National City, PNC, and Alliance One) to avoid additional surcharges

- No fees: Initial card issuance, monthly paper statements, purchases at point of sale locations (PIN or signature), cashback with purchase, monthly maintenance

- One free ATM balance inquiry per deposit each month at Charter One Bank or SHAZAM Privileged Status locations; otherwise, $0.50 per inquiry

- One free ATM cash withdrawal per deposit each month at Charter One Bank or SHAZAM Privileged Status locations; thereafter $1.35 per withdrawal

- One free unused ATM withdrawal will rollover to next calendar month

- ATM denial for insufficient funds: $0.50 each time

- Deposit transfer to another bank account: $1.50 each transfer

- One free card replacement per year; thereafter, $4.00; expedited delivery of card costs $15.00

- International currency conversion, 3%; international cash/purchase, 3%29

Utilization of third party vendors

- Comerica Bank

Program: Child support payment disbursements

Type: G2P

Agency: State Disbursement Unit, Department of Healthcare and Family Services

Description: Program collects payments from noncustodial parents, including voluntary and court-ordered garnishments through their employers, and disburses those payments to custodial parents

Options for making child support payments

- Direct deposit (ExpertPay.com)

- It takes about 2 to 4 weeks for direct deposits to start. In the meantime, paper checks are sent

- Debit card (Way2Go Cards)

- Paper check

Volume of payments (2018)

Costs/fees/surcharges

- Direct deposit and paper check, no cost to custodial parent receiving payment

- Recipient costs for receiving payments by debit card30

- No monthly fee, enrollment fee, set-up fee, in-state ATM balance inquiry fee

- No fees for ATM withdrawals in Illinois, $3.00 fee for out-of-state ATM withdrawals plus an additional surcharge depending on the bank

- $0.50 fee for ATM out-of-state balance inquiry

- Teller-assist cash withdrawal, $2.25

- Point of sale denial, $0.75

- Bill pay, $1.00

- Card replacement, $5.00; Expedited card delivery, $15.00

- Funds transfer via interactive voice response phone or web portal, $1.50

- Mobile balance inquiry, one free per deposit, $0.10 for each thereafter

- Annual cost of contract: $8,191,920 (Contract: #915KSDU0001)31

Utilization of third party vendors

- Conduent, Inc. (Conduent State & Local Solutions and Conduent Business Services)

- ComericA Bank through Conduent for debit card

Program: Personal assistants of the Home Service Program

Type: G2P

Agency: Department of Human Services, Division of Rehabilitation Services

Description: Helps individuals with disabilities under the age of 60, unless in the AIDS or Brain Injury Medicaid Waiver Programs, to achieve independent living so that these individuals may remain in their homes. The recipients are allowed to hire their own personal assistants who provide household tasks, personal care and some physician-approved healthcare procedures. The Division pays the personal assistants, except for certain relatives who are ineligible for payments.

Payment recipients

- Division of Rehabilitation Services Personal Assistants

Payment options

- Direct deposit

- Paper Check

- Illinois Debit MasterCard32

Volume of payments (2018)33

- Direct deposit: $218,200,394.14 (46%)

- Paper check: $143,695,616.89 (30%)

- Debit card: $110,053,984.31 (23%)

Costs/fees/surcharges

- Recipient costs for receiving payments by debit card

- Recipients are encouraged to use ATM locations with certain brands (Charter One, Privileged Status, National City, PNC, and Alliance One) to avoid additional surcharges

- No fees: Initial card issuance, monthly paper statements, purchases at point of sale locations (PIN or signature), cashback with purchase, monthly maintenance

- One free ATM balance inquiry per deposit each month at Charter One Bank or SHAZAM Privileged Status locations; otherwise, $0.50 per inquiry

- One free ATM cash withdrawal per deposit each month at Charter One Bank or SHAZAM Privileged Status locations; thereafter $1.35 per withdrawal

- One free unused ATM withdrawal will rollover to next calendar month

- ATM denial for insufficient funds: $0.50 each time

- Deposit transfer to another bank account: $1.50 each transfer

- One free card replacement per year; thereafter, $4.00; expedited delivery of card, $15.00

- International currency conversion, 3%; international cash/purchase, 3%34

Utilization of third party vendors

- Comerica Bank

Program: Lottery

Type: G2P

Agency: Department of the Lottery

Description: Utilizing a private management company to implement, regulate and ensure the integrity of state lottery games, the Lottery runs games of chance to raise revenue for the state.

Payout methods

- Lottery retail outlets (winnings less than $600): cash

- Prize claim centers (between $600 and $25,000): paper check only

- Comptroller (over $25,000): paper check or direct deposit

Volume of winning payouts (2018)

Utilization of third party vendors

- Camelot Illinois, LLC., for private management

Program: SNAP, a.k.a. food stamps

Type: G2P

Agency: Department of Human Services

Description: Provides assistance to eligible households for the purchase of food through pre-approved vendors.

Payment options

- Illinois Link Card (EBT card)

Volume of payments35

- In 2018, a monthly average of 1,803,885 persons in 901,460 SNAP households received total annual benefits of $2,738,038,834.36

- All payments are through the Link Card

Costs/fees/surcharges

- Client EBT card costs

- No charge for using Link Card at point-of-service terminals

- Clients are allowed two free withdrawals at ATMs per calendar month. Thereafter, there is a $1 transaction fee.

- Clients are allowed two free balance inquiries at ATMs per calendar month. Thereafter, there is a $0.50 transaction fee.

- Annual cost of contract: $7,797,00037

Utilization of third party vendors

- Conduent, Inc. per Link III comprehensive contract

Program: State employee payroll

Type: G2P

Agency: Office of the Comptroller

Description: Payroll of state employees jointly approved by the comptroller and the treasurer

Payment options

- Direct deposit (default)

- Paper check ($2.50 processing fee unless meets one of the exceptions)

Volume of payments (2018)

- A monthly average of 63,881 employees

Costs/fees/surcharges

- None for direct deposit

- Comptroller is statutorily authorized to charge $2.50 for each paper paycheck

- For most cases, the $2.50 fee is charged.

- Exceptions: certain union contracts, first-time pay, hardship exemptions

- Over a 12 month period, the comptroller collected $75,600 for the $2.50 fee.

- The Office of the Comptroller does not have a cost estimate for paper check writing.

Utilization of third party vendors

There are about 10 payroll processors that submit payroll vouchers to the comptroller. Once approved, the comptroller and treasurer electronically co-sign the “checks” so the payroll payments may go out.

Program: Tax refunds

Type: G2P

Agency: Department of Revenue

Description: Disbursement of tax refunds

Disbursement options

- Direct deposit

- Paper check

- Debit card (individual income tax only)38

Volume of refunds (2018)

Debit card costs39

- For taxpayer: no monthly fee, per purchase fee, in-network ATM withdrawal fee, cash reload fee, or customer service fee.

- ATM balance inquiry fee: $0.50

- Inactivity fee: $1.50 per month after 365 days of inactivity

- One free card replacement per year; thereafter $7.50 and $15 for expedited delivery

Utilization of third party vendors

- KeyBank (for debit card refunds for individual income taxpayers)

Program: Unemployment insurance

Type: G2P

Agency: Department of Employment Security

Description: Provides unemployment insurance payments to unemployed persons

Payment options

- Debit card (default unless recipient registers for direct deposit)

- Direct deposit

Volume of payments (2018)40

- Direct deposit: 228,941 claimants (66%) received $1,153,919,012 (67%)

- Debit cards: 117,940 claimants (34%) received $576,959,500 (66%)

Costs/fees/surcharges41

- Direct deposit: no cost to beneficiaries

- Debit card costs to beneficiaries:

- No charge for U.S. card purchases, declined card purchase, ATM balance inquiries, automated or live agent customer service balance inquiries, online or mailed paper transaction history, text message and email alerts, or inactivity

- Two free monthly ATM withdrawal transaction at KeyBank and Allpoint; $1.40 per transaction thereafter

- Two free monthly ATM withdrawals at all other locations; $1.40 per transaction thereafter

- International ATM withdrawal–$2.75 per transaction

- One monthly free over-the-counter withdrawal at participating MasterCard member bank branches participating ; $5.00 thereafter

- $0.50 per payment per each online bill payment

- One free replacement card per year; $7.00 thereafter; overnight delivery, $14.50

- Account expires in two years; paper check issued for balance, $12.00

- No cost to the department for issuing the debit card

Utilization of third party vendors

- KeyBank

Program: Workers’ compensation

Type: N/A

Agency: Workers’ Compensation Commission

Description: Provides compensation to workers covered by workers’ compensation insurance due to a work-related incident

Note

Workers’ compensation is included in this study because it was included in the electronic payment disbursement survey by the Council of State Governments report Cash-less State Governments.42 However, workers’ compensation benefits in Illinois are paid by the insurer carrying the workers’ compensation policy for the employer or by the employer if the employer is self-insured. All self-insured employers require governmental approval. Therefore, workers’ compensation in Illinois is not an area where state government plays a meaningful role when it comes to the method of payment used and is not tabulated in the results of this study.

Catalog of Collections by Major Program

Program: All Kids co-insurance premium collections

Type: Person payment to government, P2G

Agency: Department of Healthcare and Family Services

Description: All Kids is Illinois’s Separate Child Health Insurance Program, or CHIP. It provides health insurance for children, defined as age 18 or younger, whose family’s income, as measured by the Modified Adjusted Gross Income, or MAGI, standard, exceeds the income threshold for Medicaid, currently set at 142% of the federal poverty level, up to 313% of the federal poverty level. All Kids divides families into four categories based on income. The upper two categories – Premium Level 1 and Premium Level 2 – require co-insurance payments to participate in the All Kids program. Premium Level 1 requires monthly premiums of $15 for the first child enrolled, $25 for 2 children, increasing by $5 per child up to a maximum of $40 per month. Premium Level 2 requires monthly premiums of $40 per child or $80 for more than two children.43

Payment options44

- Monthly deductions from a checking account

- Electronic deduction from bank account to make one-time payment

- Credit/debit card payment using the treasurer’s E-Pay Program

Volume of collections45

Costs/fees/surcharges46

- No fees are passed on to clients. The department absorbs them all.

- The department pays $0.08 per deposit from bank account and 1.45% of the transaction amount credit/debit card deposits costing $22,389 in 2018.

Utilization of third party vendors

- Forte, transitioning to JetPay per the treasurer’s ePAY Program

Program: Child support payment collections

Type: P2G

Agency: State Disbursement Unit, Department of Healthcare and Family Services

Description: Program collects payments from noncustodial parents, including voluntary and court-ordered garnishments through their employers, and disburses those payments to custodial parents.

Options for making child support payments

- Direct deposit (ExpertPay.com)

- Credit/debit card (online through e-childspay.com or by phone)

Volume of payments (2018)47

- Direct deposit: 802,393 (89.5%) total payments totaling $136,327,025 (95.2%)

- Online/pay-by-phone: 40,370 (4.8%) total payments totaling $15,942,238 (10.5%)

Costs/fees/surcharges48

- For credit/debit card payments, $14.95 per $0.01 to $500 payment; 2.95% for payments over $500.

- For direct deposit, one-time registration fee of $2.50 to verify account information.

- Annual cost of contract: $ 8,191,92049

Utilization of third party vendors

- Conduent, Inc. (Conduent State & Local Solutions and Conduent Business Services)

Program: Office of the Secretary of State fee collections

Type: P2G

Agency: Office of the Secretary of the State

Description: Unique among the states, the Illinois secretary of state collects a wide range of fees, from archive fees to business services fees, vehicle fees and driver fees.

Payment options

- Paper check

- Credit/debit card

- Cash

Volume of fee collections (2018)

Costs/fees/surcharges50

- No charges to fee payers if they pay by direct deposit, paper check, or cash.

- If fee payers pay by credit/debit card, they pay a 2.25% transaction fee with a $1.00 minimum

Utilization of third party vendors

- Forte, transitioning to JetPay per the treasurer’s ePAY Program

Program: Tax collection

Type: P2G

Agency: Department of Revenue

Description: Collection of taxes

Payment options

- Direct deposit

- Paper check

- Credit/debit card (all but for business/corporate taxes)

- Cash (all but for business/corporate taxes)

Volume of collections by payment method (2018)51

Note: GenTax is a system that allows Illinois to collect multiple taxes from the same taxpayers. However, the department stated it is unable to break out the various taxes. It can be any of the taxes collected, and from any taxpayer.

Costs/fees/surcharges52

- Taxpayers pay convenience fees by credit card service vendors as follows:

- Official Payments Corporation (OPC), Value Payments Systems (VPS) and Link2Gov (FIS): no more than 2.49% by contract

- Treasurer’s ePAY Program: Forte, 2.35%; JetPay, 2.15%

- No other costs to the department

Utilization of third party vendors53

- OPC (Income Tax)

- VPS (Income Tax)

- FIS (Income Tax)

- In Springfield and Forte, transitioning to JetPay per the treasurer’s ePAY Program

Endnotes

- The inflows of money examined in this report are $48.6 billion in collections, including payments for tax liabilities, fees, fines, shared payment for services, and money received when state government acts as an intermediary payment facilitator. These collections do not include grant money, such as grants from the federal government. The outflows of money examined in this report are $14.3 billion in disbursements, which are highlighted when the state government acts as a tax collector, refunder, lottery winnings cashier, employer, procurer, contracting-out service provider, direct welfare benefactor, indirect welfare benefactor and intermediary payment facilitator.

- Dwight V. Denison, Merl Hackbart, and Juita-Elena (Wie) Yusuf, “Electronic Payments for State Taxes and Fees: Acceptance, Utilization, and Challenges,” Public Performance & Management Review, Vol. 36, No. 4, June 2013, pp. 616–636.

- Dwight V. Denison and Saerim Kim, Cash-less State Governments: Electronic Collections and Benefit Disbursements, Research for the Council of State Governments Financial Service Working Group, 2018 https://issuu.com/csg.publications/docs/epayments_report_online.

- The Council of State Governments study provided a list of programs that use cashless payment options, and that list was used as an initial basis to identify important governmental programs in Illinois that disburse funds, including governmental functions such as refunding tax overpayments and payroll. In order to collect the data and ascertain other information, requests were sent to Illinois state agency officials.

- Office of the Illinois State Comptroller website: Direct Deposit Sign Up: https://illinoiscomptroller.gov/vendors/direct-deposit-sign-up, accessed August 23, 2019.

- Illinois Constitution, Article V §§ 1, 17, and 18.

- 15 ILCS 505/7

- 15 ILCS 405

- 15 ILCS 405/9

- “The comptroller, with approval of the treasurer, may provide by rule or regulation for direct deposit of any payment lawfully payable from the state treasury” to agencies for the disbursement of payments for the following groups: 1) Persons paid from personal services [Home Service Program] 2) Persons receiving payments under state pension systems 3) Individuals who receive assistance under Articles III [Aid to the Aged, Blind or Disabled], IV [Temporary Assistance for Needy Families], and VI [General Assistance] of the Illinois Public Aid Code 4)Providers of services for those with mental health and development disabilities under the Mental Health and Developmental Disabilities Administration Act 5)Providers of community-based mental health services 6)Providers of services under programs of the State Board of Education

- Civil Administrative Code of Illinois, Department of Revenue Law: 20 ILCS 2505/2505-210

- The first four of these considerations are commonly found in payments literature and were identified as top state official concerns during the research for the Association of Government Accountants: Helena G. Sims and Steven E. Sossel, “Government Prepaid Cards Lower Costs and Improve Access,” Corporate Partner Advisory Group Research Series, Rep No. 34, Association of Government Accountants, June 2013, p. 15.

- Sims, pp. 4-5.

- “2017 FDIC National Survey of Unbanked and Underbanked Households,” Federal Deposit Insurance Corporation: https://www.economicinclusion.gov, accessed October 7, 2019.

- Sims, pp. 16, 24.

- Ibid.

- This observation came from interviews with officials of the Office of the Comptroller and justifies further inquiry into why local governments insist on receiving payments by paper checks.

- According to Sims, p. 11: “Florida was the first state to request such a revenue-sharing arrangement.” The study also mentioned California as another state with similar revenue-sharing arrangements.

- Ibid, p. 16.

- For example, Regulation E of the Federal Reserve regulates electronic funds transfers and debit cards, and Regulation P regulates the privacy of consumers serviced by financial institutions. Also, see National Consumer Law Center, “New Protections for Prepaid Cards and Accounts,” March 28, 2019: https://www.nclc.org/images/pdf/high_cost_small_loans/prepaid-card-accounts-ib.pdf

- Office of the Treasurer FOIA request responses, August 2019 and Treasurer webpages on ePay: https://illinoistreasurer.gov/Local_Governments/ePAY_Overview, accessed August 12, 2019.

- For further information of EBT requirements for the food stamp program, see Food and Nutrition Service, Electronic Benefits Transfer (EBT) Request for Proposal (RFP) Guidance, Version 2.0, December 19, 2007

- Sims, p. 5.

- The rough estimate of more than $1 million is based on some known quantities mixed with unknown factors. For example, it is known that there are 874,102 paper checks issued to custodial parents for child support in 2018. However, lacking an estimated cost per each check in Illinois, the federal cost of approximately $1 per check can be used as a proxy.

- A fertile area for research is a closer examination of vendor payments, especially paper checks, and other state government costs not captured by this study.

- Contract #981AQ164000 that combines SNAP with cash program, Illinois State Comptroller Financial Data: State Contracts, online system: https://illinoiscomptroller.gov/index.cfm/financial-data/state-expenditures/contracts/, accessed August 13, 2019.

- Illinois Department of Human Services website: DHS>for Providers/Payments>Illinois Debit Master Card: http://www.dhs.state.il.us/page.aspx?item=45466, accessed August 6, 2019.

- Department of Human Services FOIA request response.

- Illinois Department of Human Services website: DHS>for Providers>Payments> Illinois Debit MasterCard>Getting Started>Fee: http://www.dhs.state.il.us/page.aspx?item=45470, accessed August 6, 2019.

- Illinois Disbursement Unit Way2Go Card application, https://www.ilsdu.com/includes/docs/Way2GoCardEnrollmentForm.pdf, accessed August 6, 2019.

- Illinois State Comptroller Financial Data: State Contracts, online system. https://illinoiscomptroller.gov/index.cfm/financial-data/state-expenditures/contracts/, accessed August 13, 2019.

- Illinois Department of Human Services website on Illinois Debit Master Card.

- Department of Human Services FOIA request response.

- Illinois Department of Human Services website on Debit MasterCard Fee.

- Department of Human Services FOIA request response.

- Food & Nutrition Services, U.S. Department of Agriculture, SNAP Program Data by State.

- Contract #981AQ164000.

- Department of Revenue website, Revenue>Questions and Answers>KeyBank Debit Card FAQ’s: https://www2.illinois.gov/rev/questionsandanswers/Pages/keybankdebitcard.aspx, accessed August 6, 2019.

- Department of Revenue website: Key2Prepaid KeyBank debit card information: https://www2.illinois.gov/rev/individuals/Documents/keybankdebitcardinformation.pdf, accessed August 6, 2019.

- Department of Employment Security FOIA request responses, August 2019.

- Department of Employment Security webpage on Key2Benefits Schedule of Card Fees (https://www2.illinois.gov/ides/IDES%20Forms%20and%20Publications/debitcard_fees.pdf), accessed August 13, 2019, and department FOIA request responses, August 2019.

- Denison and Kim, pp. 4, 15, 26, 28 and 35.

- Department of Healthcare and Family Services webpage on All Kids Cost: https://www.illinois.gov/hfs/MedicalPrograms/AllKids/Pages/income.aspx, accessed August 13, 2019.

- Department of Healthcare and Family Services webpages on electronic payments: https://www.illinois.gov/hfs/MedicalPrograms/AllKids/Pages/payments.aspx, https://www.illinois.gov/hfs/MedicalPrograms/AllKids/Pages/epay.aspx

- Department of Healthcare and Family Services FOIA request responses, August 2019.

- Ibid.

- Ibid.

- Department of Healthcare and Family Services webpages on child support payments, https://www.illinois.gov/hfs/ChildSupport/parents/Pages/ElectronicPayments.aspx, accessed August 15, 2019.

- Contract #915KSDU0001,Illinois State Comptroller Financial Data: State Contracts, online system. https://illinoiscomptroller.gov/index.cfm/financial-data/state-expenditures/contracts/, accessed August 13, 2019.

- Ibid.

- Department of Revenue FOIA request responses, August and September 2019.

- Ibid.

- Ibid.